Social Listening for Fintech: A Practical Guide to Audience and Narrative Intelligence

Social listening for Fintech is the practice of analysing real-time public conversation across social media, forums, news, and financial communities to understand how people experience money, risk, and trust in a digital economy. For Fintech brands, these conversations shape adoption, reputation, and regulatory scrutiny long before they appear in dashboards or earnings calls.

As financial services move faster than consumer understanding, social listening has become a form of audience and narrative intelligence. It reveals how different communities — from venture capitalists and crypto enthusiasts to financially vulnerable users — interpret products such as digital wallets, Buy Now Pay Later, and AI-driven customer service. Beyond tracking mentions, Fintech social listening surfaces the emotional drivers behind behaviour: anxiety during market volatility, scepticism toward institutions, and the growing expectation that financial brands should educate as well as transact.

By combining social listening with audience and narrative intelligence, Fintech organisations can move from reactive reputation management to proactive strategy — identifying emerging risks, validating product use cases, and aligning innovation with the cultural and psychological realities shaping financial decision-making.

Critical Insights for Fintech

The following insights represent the core realities of the Fintech landscape in 2025 and 2026, derived from large-scale audience analysis and market data:

- Reputation Velocity: The speed of information diffusion on social media has created a "digital bank run" dynamic, where niche community anxiety can escalate into institutional collapse within hours.

- Contextual Evolution: Fintech products often evolve faster than their marketing. Social listening reveals that tools like Buy Now, Pay Later (BNPL) have shifted from being lifestyle luxuries for Gen Z to survival lifelines for a broader demographic during the cost-of-living crisis.

- The Profitability Pivot: The industry has moved beyond a "growth-at-all-costs" phase into a maturity cycle; according to Boston Consulting Group (BCG) as of 2024, 69% of publicly listed Fintech firms reached profitability, heightening the need for efficient, data-driven customer retention strategies.

AI as the New Standard: According to the World Economic Forum, 80% of Fintech firms are now implementing artificial intelligence across business domains, with 91% either using or planning to use AI for customer service and automation, making narrative intelligence regarding AI a competitive differentiator.

Why Social Listening Is Now Essential for Fintech Brands

Social listening for Fintech brands has become essential as traditional market research struggles to keep pace with real-time shifts in consumer trust, risk perception, and financial behaviour. In a fragmented digital landscape where financial advice circulates across social media, forums, and creator-led communities, reputation is shaped less by press coverage and more by fast-moving public narratives that can influence adoption and stability within hours.

By applying social listening as audience and narrative intelligence, Fintech teams can move beyond reactive monitoring to anticipate emerging use cases, detect early signs of anxiety around fraud or regulation, and respond before issues escalate into reputational or operational risk. These insights surface well ahead of sales data or survey research.

As competition expands to include neobanks, Big Tech, and decentralised platforms, social listening also strengthens competitive intelligence. By analysing sentiment and narrative dominance — rather than mention volume alone — Fintech brands can identify positioning gaps, benchmark against competitors, and adapt product and messaging strategies with greater precision.

The Fintech Landscape: Use Cases and Examples

The strategic application of social listening in Fintech requires a granular understanding of how different communities interact with financial concepts. By applying the findings from our primary research reports, brands can operationalize audience intelligence across product, brand, and risk functions.

Product Innovation: The "Buy Now, Pay Later" Evolution

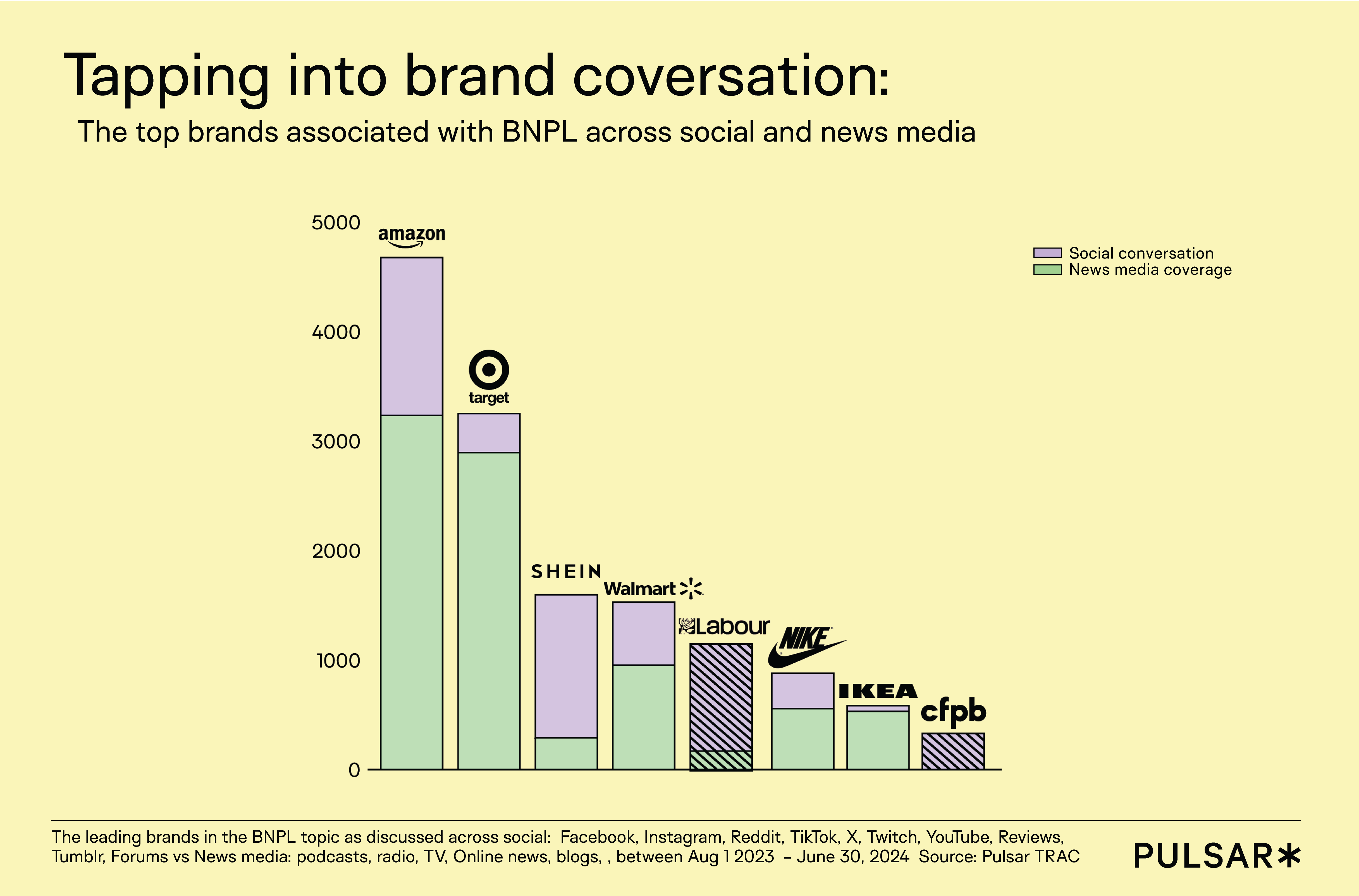

In our Buy Now Pay Later report, we analyzed the conversation surrounding major platforms such as Klarna, Afterpay, and Affirm. The research uncovered a fundamental pivot in user behavior that carries significant implications for Fintech product teams. While these services were originally discussed as tools for e-commerce "luxuries"—primarily in fashion and beauty—the conversation has moved toward using them for "survival" necessities like groceries, healthcare, and utility bills.

This evolution highlights the concept of Contextual Intelligence. Social listening allows Fintech brands to witness real-time use cases that often contradict their intended brand positioning. The analysis identified two distinct and conflicting narratives that product teams must manage. "Fintech Enthusiasts" (or "Fintechies") discuss BNPL in the abstract, focusing on market innovations, company valuations, and AI efficiency in platforms like Klarna. Conversely, "Political Science Enthusiasts" (Poli-sci Enthusiasts) drive a narrative focused on the welfare of "financially vulnerable" consumers, spark conversations about "phantom debt," and advocate for government regulation to prevent debt spirals.

For Fintech brands, the practical takeaway is the need to navigate the fine line between "empowering consumers" and "predatory lending." By monitoring these specific audience clusters, brands can act as "financial wellness" partners, developing features like transparent micro-loans or secured credit lines as safer alternatives for those in economic distress.

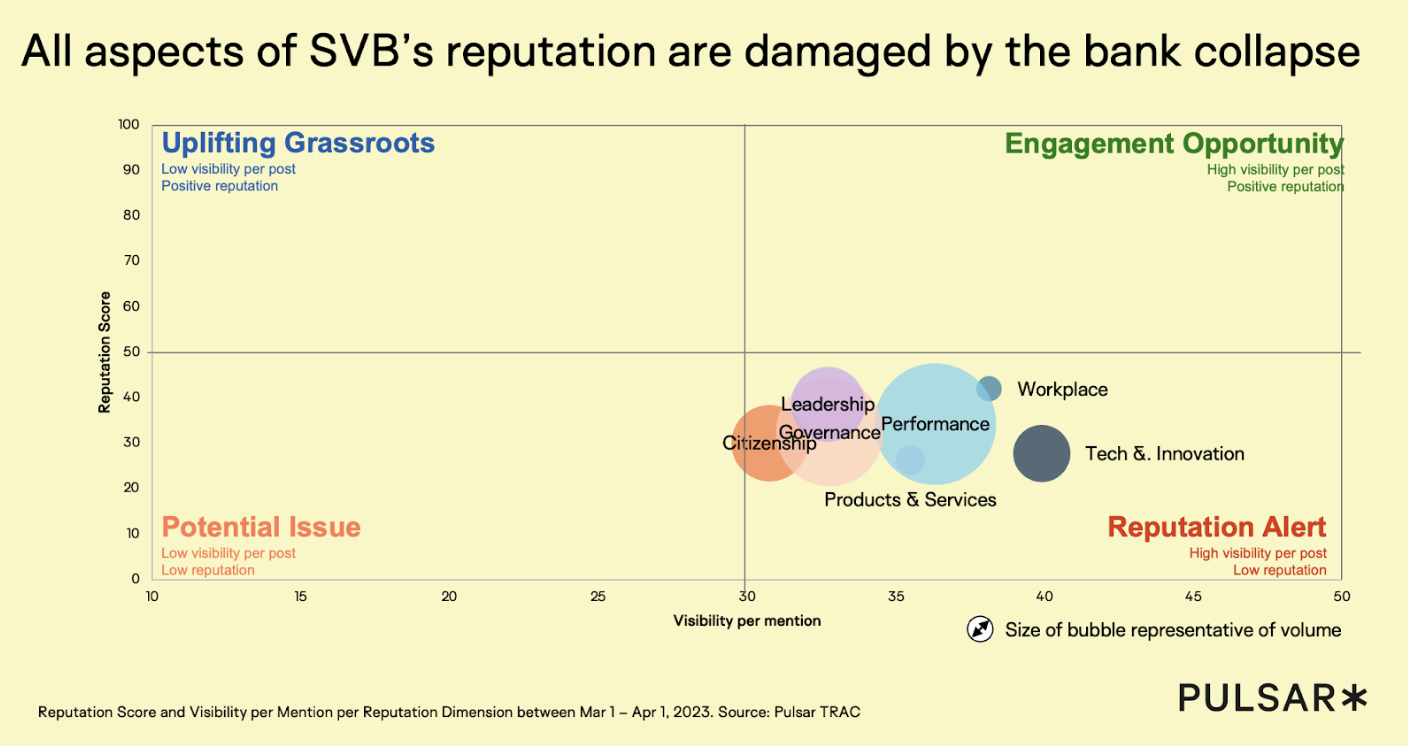

Crisis Dynamics: The Silicon Valley Bank Reputation Collapse

The collapse of Silicon Valley Bank (SVB) stands as a landmark case study for the Velocity of Reputation. In our SVB Reputation Crisis report, we mapped how the panic began in niche "Tech Startup" and "VC" communities on X/Twitter before exploding into the mainstream. This was the first bank run fueled by the velocity of social media, where a crisis evolved from niche concern to institutional collapse in minutes rather than days.

The analysis revealed that different political and social communities framed the blame through their own ideological lenses. "US Conservatives" attributed the failure to "woke" policies and diversity initiatives, while "Progressives" focused the blame on deregulation.3 This fragmentation of blame demonstrates that Fintechs need an early-warning system that monitors specific clusters—like influential venture capitalists and tech founders—to detect signals of a "digital bank run" before they hit the general news cycle. For Fintech brands, managing a crisis means mapping narrative escalation in real-time and tailoring messages by segment to address the specific anxieties of different communities.

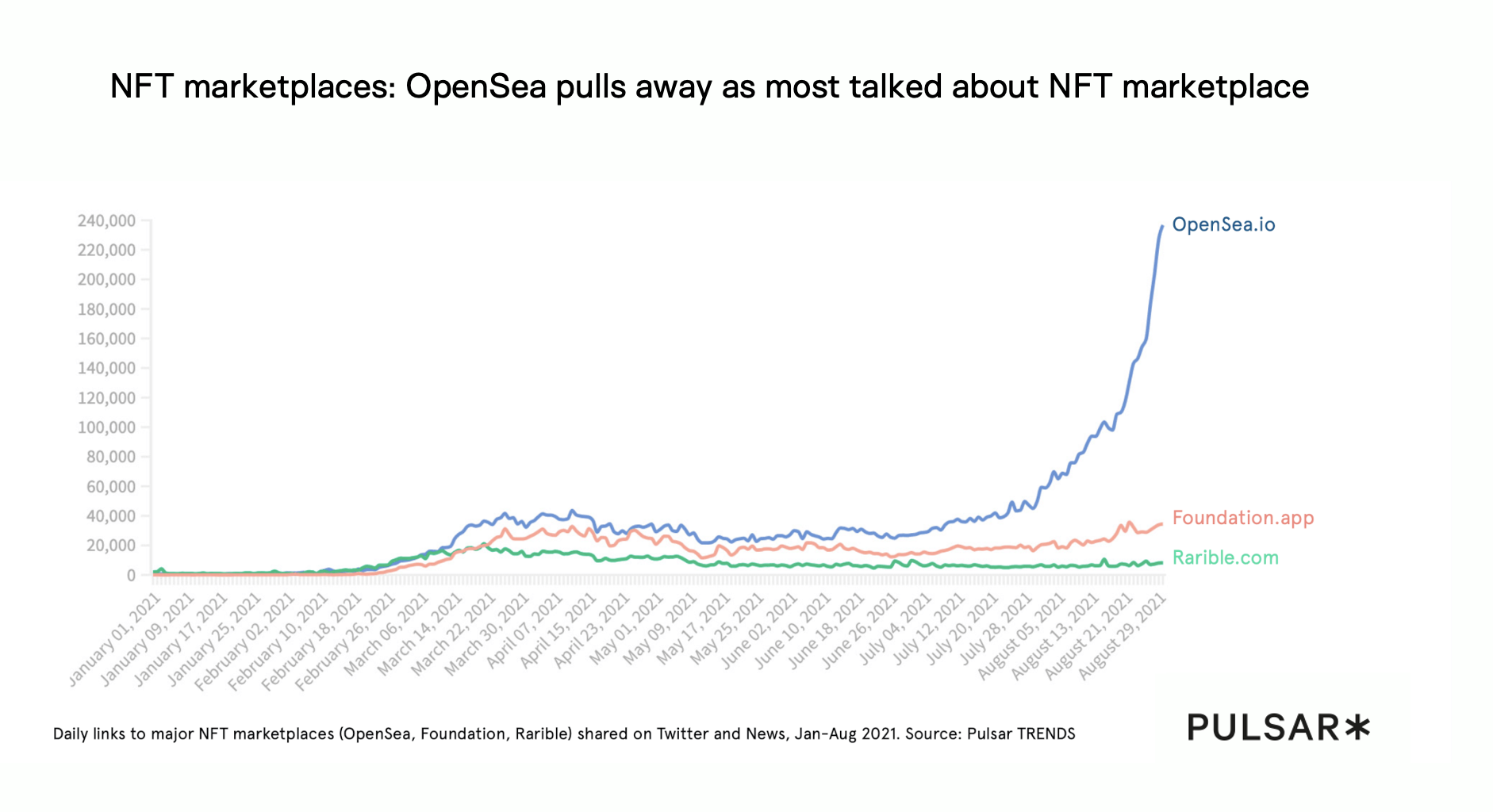

Institutional Adoption: Visa Meets CryptoPunks

When a traditional giant like Visa enters a niche cultural space, such as purchasing a "CryptoPunk" NFT for $150,000, it serves as a major signal of institutional adoption. In our NFT trends research, social listening was used to map the reaction of the digital-native community. While mainstream media often framed this as market validation, the analysis showed that niche "Wannabe VCs" and artists responded with skepticism and sarcasm, viewing it as Visa "jumping straight in" without understanding the underlying culture.

This example is critical for Fintechs attempting to co-opt emerging trends like Web3, DeFi, or AI. Social listening provides a mechanism to measure Cultural Relevance versus Appropriation. It allows legacy financial brands and new Fintechs alike to gauge if they are being welcomed as genuine innovators or mocked as "tourists." Authenticity in Fintech is not just about the transaction; it is about the "Wannabe VC" community's perception of your brand’s affinity with their values.

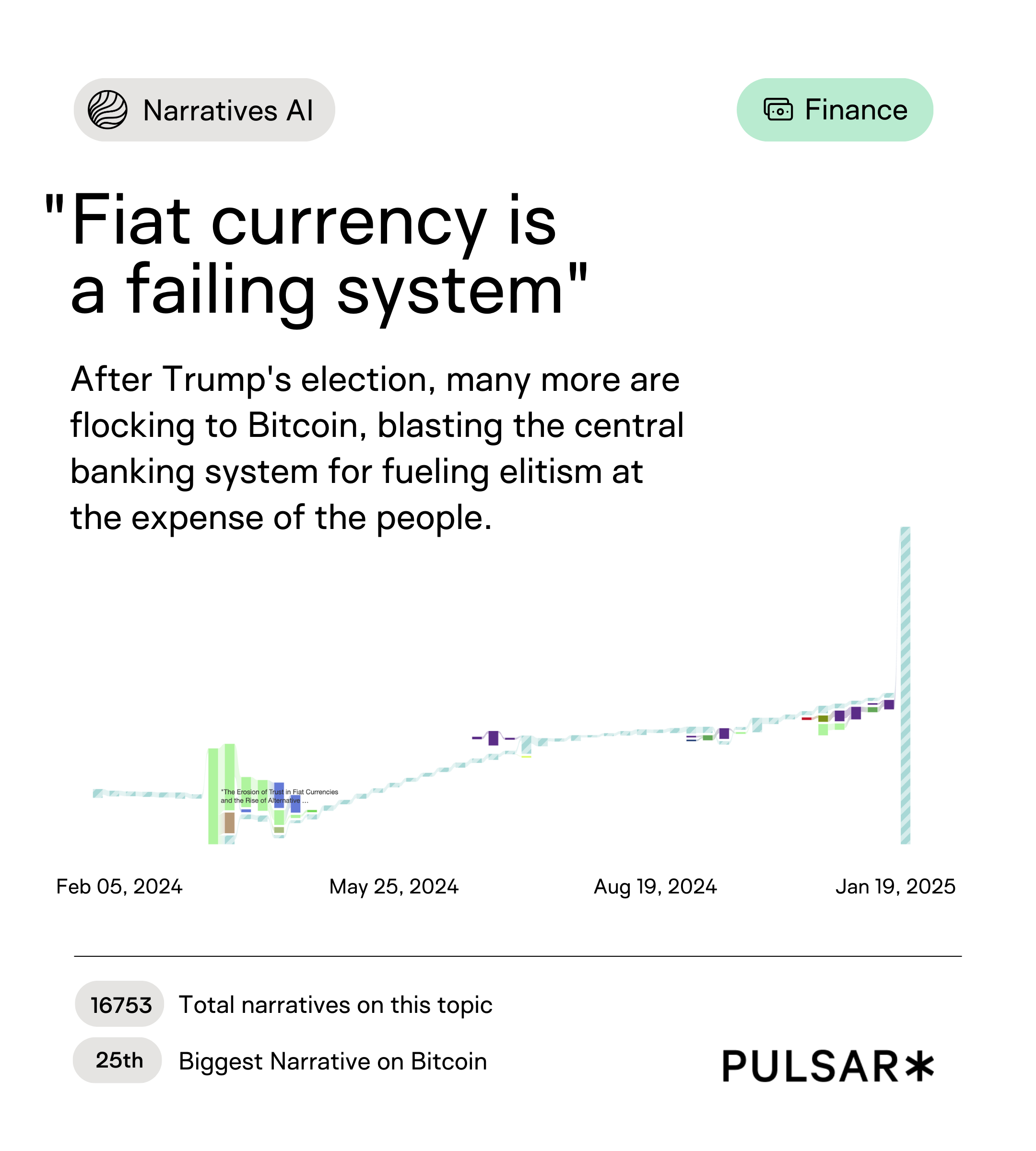

Macro-Narratives: The "Death of Fiat" Sentiment

Understanding the philosophical drivers of financial behavior is as important as understanding functional needs. In our SS2025 Narratives Report, Pulsar used Narratives AI to identify a resilient, growing macro-narrative centered on the idea that "Fiat currency is a failing system". This narrative is not merely about the fluctuating price of Bitcoin; it is a deep-seated belief system driving interest in decentralized finance (DeFi).

For Fintechs, Strategic Forecasting depends on distinguishing between functional marketing (e.g., "our payments are faster") and philosophical marketing (e.g., "our system is more ethical than central banks"). Social listening allows brands to position themselves within these macro-narratives. If a brand knows its audience consists of people who "distrust the central bank," its messaging and product roadmap should prioritize decentralization and transparency. This level of narrative intelligence ensures that Fintechs are building for the future "Accounting Spirit of Knowledge," where truth, integrity, and trust are the primary assets.

Generational Benchmarking: Gen Z and Credit Cards

The way younger generations perceive debt and rewards is fundamentally different from their predecessors. Our Credit Card Report revealed that "Young Crypto Enthusiasts" are heavily engaging with traditional credit card brands—but specifically in the context of crypto-linked rewards.

This insight is vital for Audience Acquisition. Gen Z does not view "TradFi" (Traditional Finance) and "DeFi" (Decentralized Finance) as separate silos; they expect a merged experience. While older demographics prioritize "protection" and "cashback" in their financial discussions, younger demographics are driven by "rewards" and "travel". Fintechs must segment their product messaging accordingly: focusing on fraud anxiety for older users while highlighting crypto-rewards and digital wallet integration for Gen Z.

Strategic Framework: From Data to Decision

Pulsar’s Listen → Map → Activate framework provides a strategic roadmap for turning raw social data into tangible business value in the Fintech sector.

Listen: What Signals Matter in Fintech

The "Listen" phase is about capturing the unfiltered voice of the customer across a fragmented digital world. For Fintechs, this means establishing a robust infrastructure that goes beyond tracking branded mentions to include broader industry terms, competitor strategies, and cultural conversations. Monitoring niche forums like Reddit and Discord is critical for detecting the "early sparks" of narrative shifts.

Key signals for Fintech brands include:

- Real-time behavioral signals that replace lagging surveys.

- Sentiment shifts regarding currency stability and geopolitical uncertainty.

- The frequency of specific "need state" conversations, such as using credit for essentials.

Map: How Audiences and Narratives are Structured

The "Map" phase involves synthesizing captured data into meaningful narratives. This is where the strategic "why" behind consumer behavior is unlocked. Fintech brands must analyze sentiment to understand the public tone and perform audience segmentation to identify distinct groups and their specific behaviors.

Pulsar Narratives acts as a powerful tool in this phase, connecting seemingly random data points to broader cultural beliefs—such as the "Death of Fiat" or the shift from luxury to survival in the BNPL market. Mapping allows a brand to understand the emotional and psychological landscape of its audience, moving beyond surface-level demographics to create a cohesive story.

Activate: How Insights Inform Strategy

The final step is to apply these insights to the overall business strategy. This involves translating data into actionable recommendations for marketing, communications, and product development.

Activation strategies for Fintechs include:

- Hyper-personalizing marketing campaigns based on feature resonance (e.g., miles vs. cashback).

- Adjusting product roadmaps to address unmet needs, such as adding financial literacy tools for at-risk users.

- Optimizing influencer partnerships by picking partners with real cultural pull rather than just large follower counts.

Audience Discovery as Competitive Advantage

Audience-led insight creates a sustainable competitive advantage by allowing Fintechs to move from reactive defense to proactive offense. By mapping emotional drivers and cultural shifts, brands can act decisively. In a world where executives view custom AI development as critical for competitiveness, the ability to layer human-in-the-loop narrative intelligence over AI outputs is the key to maintaining credibility.

The most effective campaigns in 2025 are those that blend earned storytelling with data-led targeting, using deeper audience intelligence like sentiment mapping and contextual trend analysis to design narratives based on emotional motivations rather than product attributes alone. This approach ensures that Fintechs are building "Trust-First Brands" that resonate on a human level.

Conclusion & Next Steps

Social listening is no longer a peripheral marketing tool; it is a strategic mindset for any Fintech brand serious about its customer experience and market survival. By understanding the velocity of reputation, the cultural nuances of adoption, and the macro-narratives driving belief systems, Fintechs can bridge the gap between their technical innovations and their users' emotional realities.

Key Takeaways:

- Reputation is Climate: Monitor the velocity of narratives to prevent niche anxieties from becoming digital bank runs.

- Context is King: Use social listening to identify when product use cases shift from luxury to survival, and adjust positioning accordingly.

- Authenticity is the Currency: Avoid cultural tourism; use audience intelligence to ensure institutional moves into new spaces (like NFTs or AI) are perceived as authentic.

- Segment for Relevance: Recognize that different generations and ideological groups frame financial value differently—Gen Z wants rewards, while "Poli-sci" enthusiasts want protection.

Bridge the Knowledge Gap: Use social insights to become a financial educator, as most consumers feel satisfied but uninformed.

To stay up to date with our latest insights and releases, sign up to our newsletter below: