Top 5 Beauty Trends on Social Media 2026

- Beauty

Beauty trends on social media in 2026 are being shaped less by product launches and more by audience behavior, platform dynamics, and cultural debate. Across TikTok, Instagram, and creator-led spaces, trends now emerge through conversation, visual experimentation, and community signaling, rather than top-down brand influence. What gains traction is defined by how beauty intersects with identity, technology, health, and value in an always-visible digital culture.

Beauty > intelligence by 2028. Looks-maxxing is just the beginning of this trend

— foks (@ExaltedFoks) December 6, 2025

Using audience intelligence and narrative analysis, Pulsar tracks how beauty conversations evolve at scale across social and media platforms. This analysis shows that the defining beauty trends of 2026 sit within clear tensions — AI innovation and mental well-being, preventative aesthetics and ethical concern, performance and naturalness, visibility and vulnerability, luxury and accessibility. The five trends explored here reflect how beauty culture is negotiating these pressures in real time, revealing what is shaping social beauty discourse now and what will matter most as 2026 unfolds.

Contents:

- AI in Beauty: Changing the Landscape

- The Normalization of Injectables: Baby Botox, Ozempic and Vampire Facials

- The Evolution of Natural Deodorant: The Compromise Economy

- Acne Acceptance: Starface, The "Cute-ification" of Flaws, and Performative Vulnerability

- Dupe Culture: The "Doop" Economy and the Death of Brand Loyalty

- Conclusion and looking ahead to 2026

1. AI in Beauty - changing the landscape

The Innovation vs. Mental Health Paradox

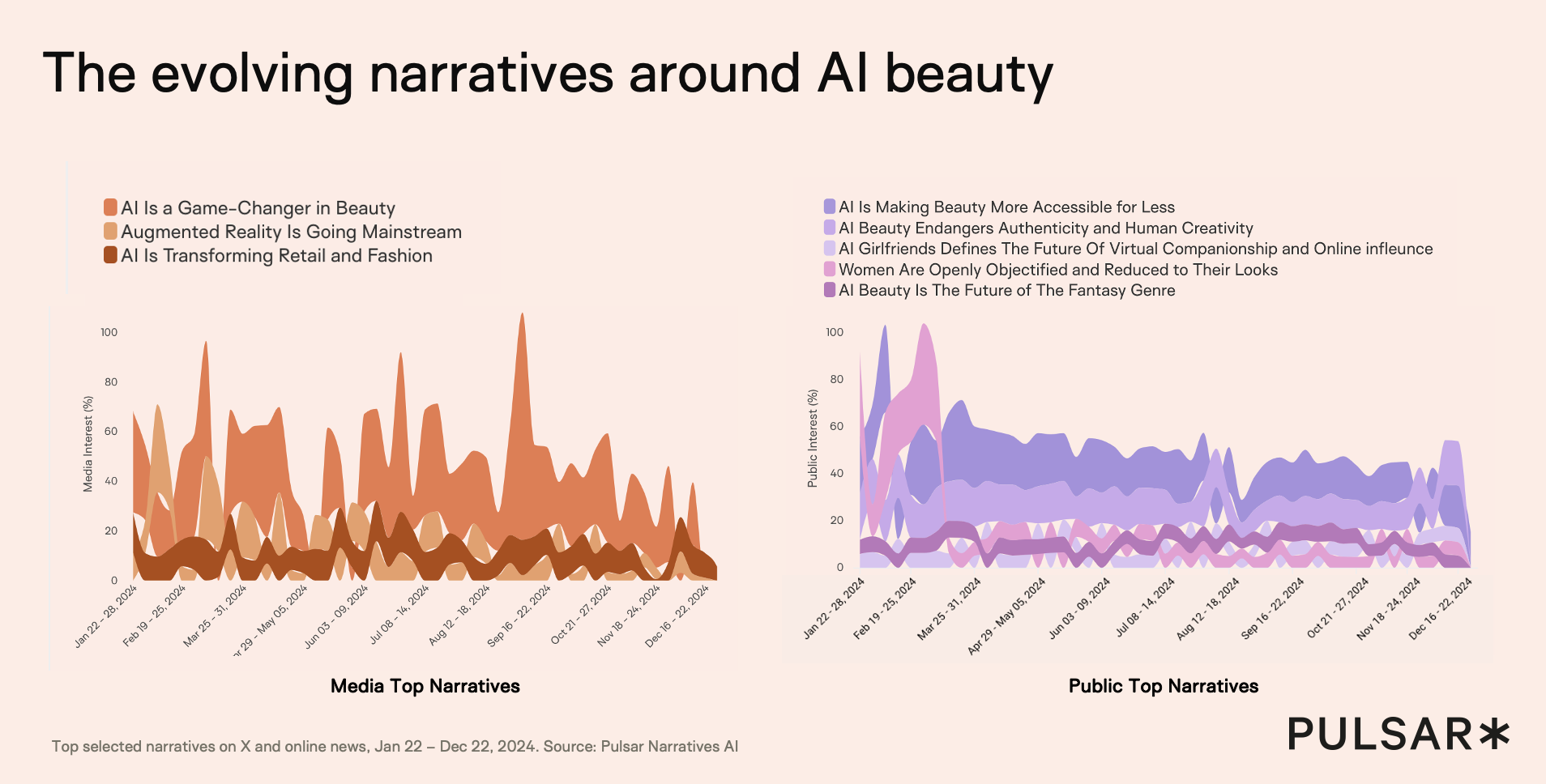

By 2026, Artificial Intelligence has ceased to be a "trend" and has become the underlying infrastructure of the beauty industry. However, as AI becomes ubiquitous, a fierce narrative battle has erupted. A comprehensive analysis by Pulsar on Beauty in an AI Age shows how beauty conversations increasingly sit at the intersection of technology, identity, and self-optimization, with AI emerging as both a creative and cultural force.

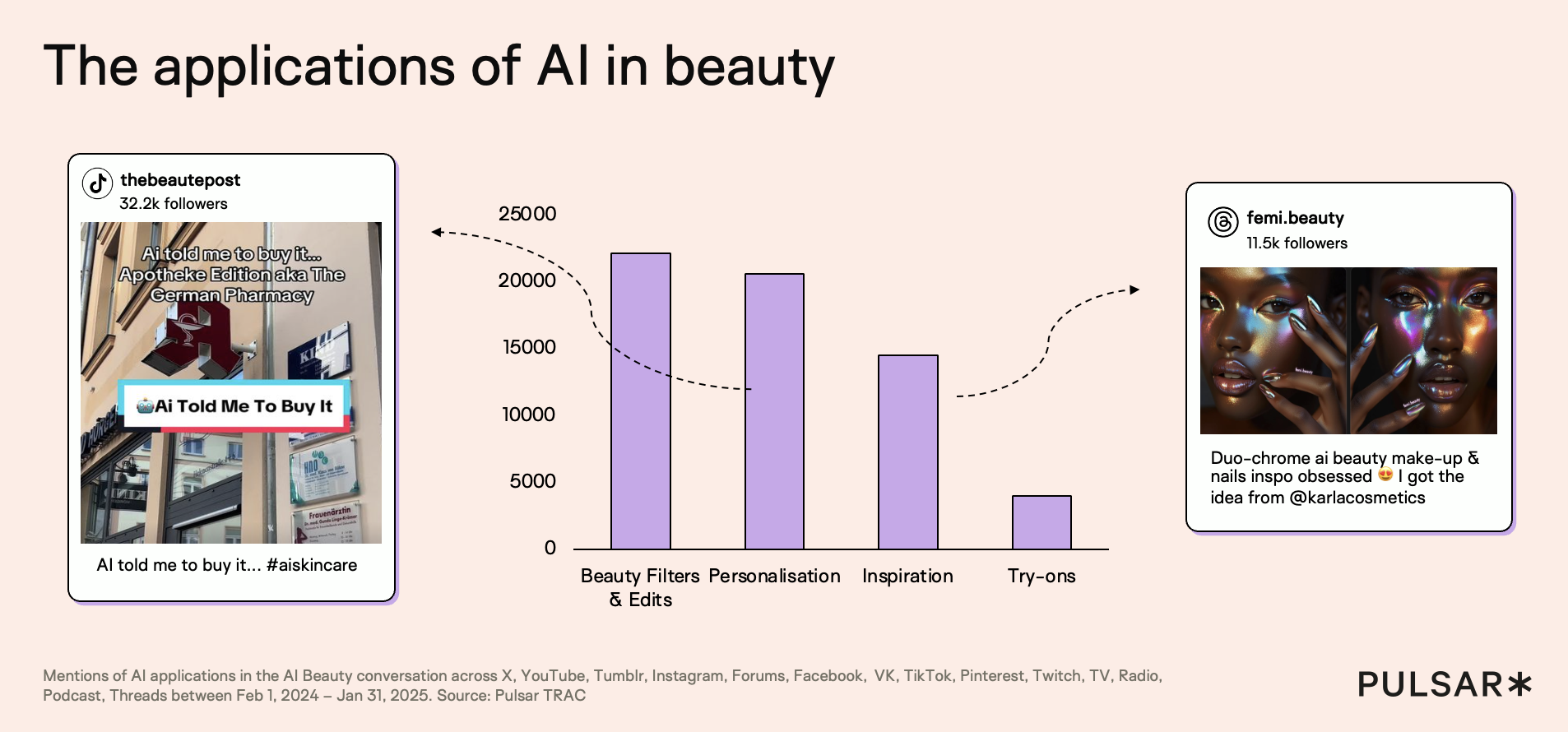

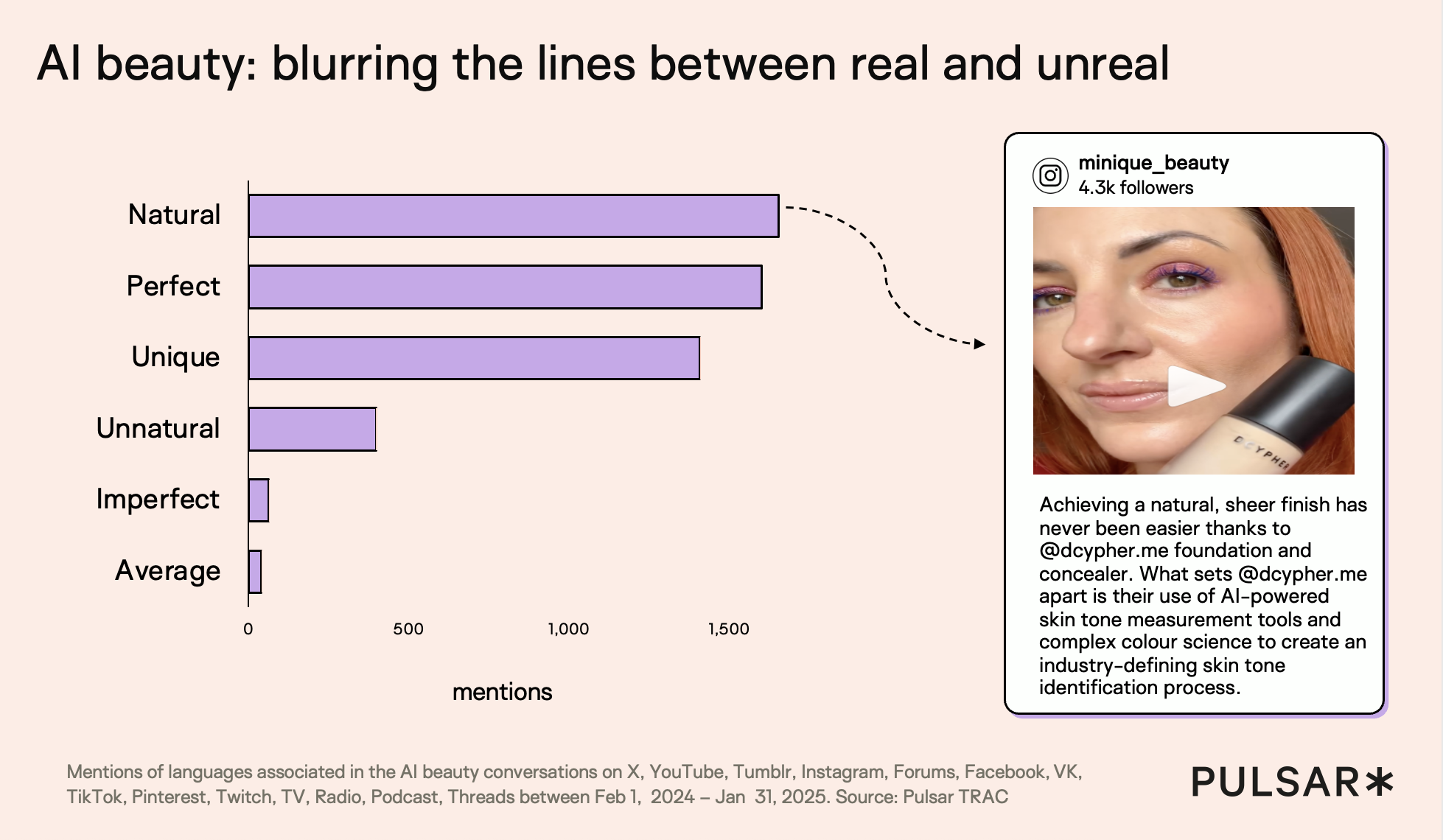

Here we see narratives in media on the left and narratives in social media on the right. Instead of one dominant look rising to the top, platforms surface multiple, parallel aesthetics tailored to micro-audiences, allowing experimental, niche, and contradictory beauty trends to thrive simultaneously. In practice, this means beauty trends move faster, fragment earlier, and feel more personal than ever before. AI is also redefining how beauty is visualized and validated on social platforms. Our report highlights the growing role of AI filters, virtual try-ons, and synthetic imagery in shaping how users imagine results before purchasing or participating in a trend.

While these tools fuel experimentation and creativity, they also intensify debates around realism, trust, and disclosure. Social conversations show audiences becoming more alert to how images are created, edited, or generated, signaling that transparency will increasingly influence which beauty trends feel credible versus performative.

At a category level, AI is pushing beauty away from static “hero products” and towards continuous, feedback-driven routines. According to the report, audiences are actively discussing AI-enabled personalization, from skin analysis tools to algorithmically tailored recommendations that adapt over time. In 2026, the most visible beauty trends will not just be looks, but systems — routines, regimens, and processes that promise responsiveness to the individual rather than conformity to a norm.

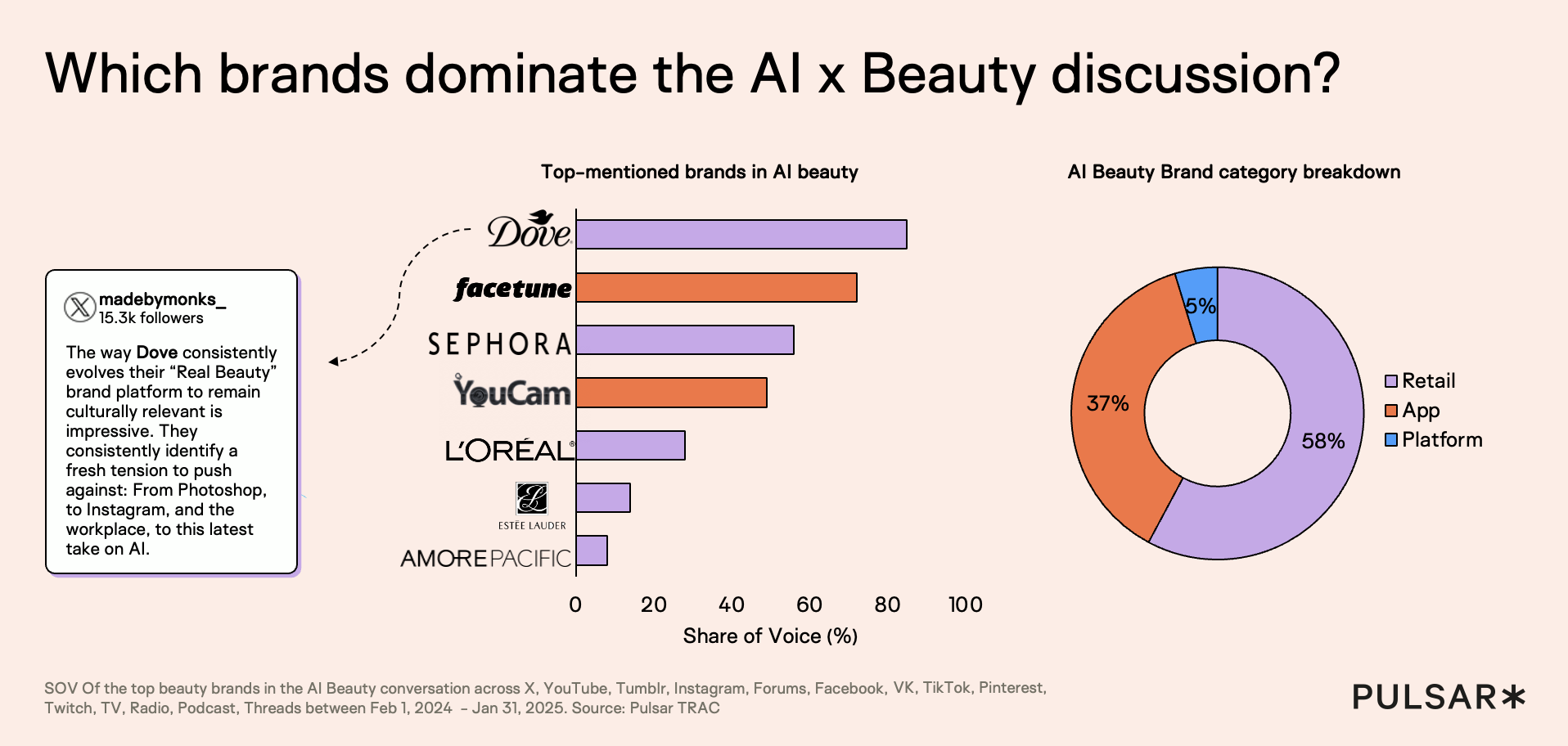

When analyzing share of voice (SoV) among top beauty brands in the AI x beauty conversation, clear leaders emerge across social, digital, and broadcast media. Between 1 February 2024 and 31 January 2025, Dove accounts for 85% of total share of voice, making it the most prominent brand associated with AI in beauty discussions. Facetune follows with a 72% share of voice, indicating that AI-powered editing and enhancement tools strongly shape how audiences understand AI in beauty. Sephora holds 56% of the conversation, highlighting the central role of retailers in AI-driven discovery and try-on experiences. YouCam captures 49% share of voice, reinforcing the dominance of virtual try-on and visualization tools, while L’Oréal appears in 28% of mentions, showing that traditional beauty manufacturers are present but less visible within AI-led beauty narratives.

How about bangs? I’m using Facetune AI. I’m obsessed with it 😂😆 pic.twitter.com/eMQ0ozaApz

— Katrina 🇺🇸🇨🇳🇲🇽 (@zapatas_mom) June 28, 2024

One specific trend set to accelerate into 2026 is the rise of AI-guided skin intelligence. Social conversations highlighted in the report point to growing interest in tools that analyze skin condition via images or data inputs and translate this into personalized care journeys. On platforms like TikTok and Instagram, this shows up as content documenting evolving routines, before-and-after diagnostics, and creator-led experiments with AI recommendations. As this trend matures, it reframes skincare less as correction and more as collaboration between user, technology, and brand — signaling a shift towards beauty trends that are adaptive, iterative, and deeply audience-led.

Key Narratives Emerging in the "AI in Beauty" Discourse:

Current consumer narratives regarding AI reveal a complex landscape of sentiment, ranging from deep anxiety about cultural impact to pragmatic acceptance of technological benefits. The following themes are driving this discourse:

- Generative Perfection: This concept drives a negative and anxious sentiment, rooted in the fear that AI filters are establishing unattainable standards, eroding self-esteem, and erasing facial diversity.

- Algorithmic Bias: Consumers remain critical of underlying data structures, expressing concern that datasets trained on Eurocentric ideals are reinforcing systematic exclusion.

- Hyper-Personalization: On a more positive and pragmatic note, there is a strong desire for efficiency, with users willing to trade their data for "products that actually work."

- Digital Authenticity: A reactionary shift is emerging, characterized by a demand for "glitchy" or "raw" content that proves humanity and explicitly rejects "polished" AI aesthetics.

The "Anti-Algorithm" Consumer

In 2026, we are seeing the crystallization of the "Anti-Algorithm" consumer segment. These individuals actively reject "AI-driven perfection," viewing imperfection as a source of value and authenticity.9 They are suspicious of "generative beauty" and are increasingly privacy-conscious, fearing data loss and the misuse of their biometric data by beauty apps.

This segment is driving the resurgence of "analog" beauty behaviors—tactile experiences, in-store consultations with human experts, and a preference for "low-tech" messaging. They are the same consumers driving the "Glitchy Glam" trend; if the AI wants symmetry, they will give it chaos.

I hope this starts a trend. If you are a beauty brand I feel like GenAI fundamentally goes against your identity. pic.twitter.com/Upibo9NBb9

— 🇵🇸 Genel Jumalon (@GenelJumalon) May 23, 2024

Strategic Implication: Brands must navigate this "Choice Architecture" carefully. While backend AI (supply chain, personalization engines) is essential for operational efficiency, frontend AI (virtual influencers, heavy filtering) carries a significant reputational risk. The winning strategy for 2026 is "AI-Enabled, Human-Verified." Brands should use AI to enhance human creativity (e.g., helping a user design their own avant-garde look) rather than replacing the human face with a synthetic ideal. Marketing campaigns must explicitly signal "No Gen-AI Used" on models to build trust with the Bio-Purist segment.

2. The Normalization of Injectables

The conversation around injectables has shifted from "correction" to "lifestyle maintenance." By 2026, procedures like Botox and fillers are as normalized as hair coloring, driven by the "Great Normalization" of medical aesthetics among Gen Z and Millennials. This is no longer about vanity; it is about "Metabolic Beauty"—the convergence of health, technology, and appearance.

The "Ozempic Face" Phenomenon & The GLP-1 Economy

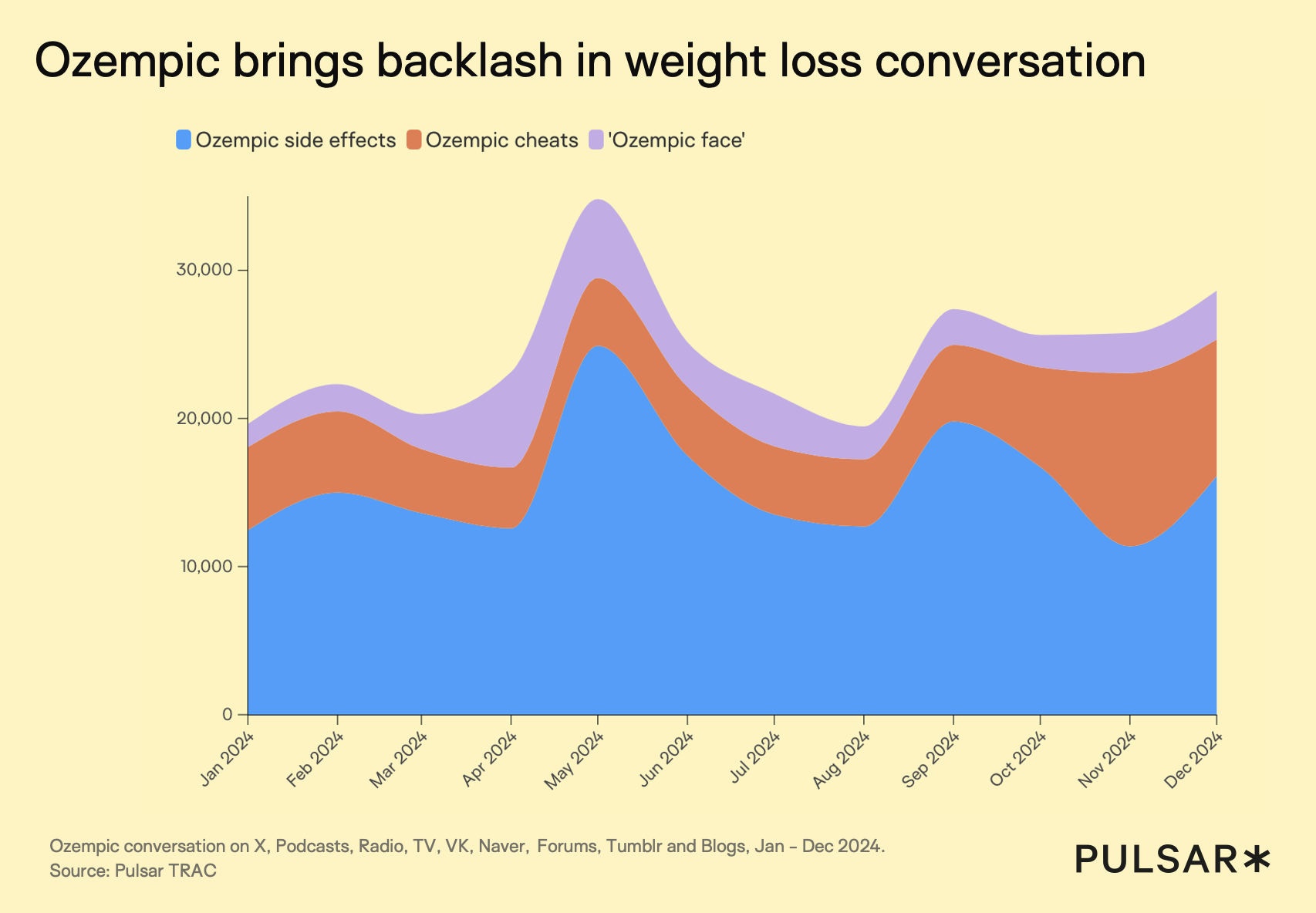

The widespread adoption of GLP-1 agonists (Ozempic, Wegovy, Mounjaro) for weight loss has created a massive secondary market in the beauty industry: the treatment of "Ozempic Face". Rapid weight loss often results in volume loss, skin laxity, and a "hollowed" appearance, which has become a primary aesthetic concern for the 2026 consumer.

Online discussion of Ozempic increasingly centers on backlash rather than weight-loss success. The dominant themes in Ozempic conversation are side effects, perceived “cheating,” and aesthetic consequences such as “Ozempic face.” Spikes in conversation suggest moments where risk narratives temporarily overtake benefit narratives. “Ozempic face” functions as a cultural shorthand for visible trade-offs of rapid weight loss. Weight-loss drug discourse mirrors beauty backlash patterns, where health optimization collides with appearance anxiety.

I’ve toyed with using Ozempic for weight loss, but the classic “Ozempic face” scares me.

— Sabeer Bhatia (@sabeer) November 9, 2025

In 2026, "Skincare for Ozempic Face" is a recognized, standalone product category. We are seeing a surge in demand for products that address the specific structural deficits caused by rapid metabolic shifts:

- Volumizing Topicals: Products containing "bio-intelligent" ingredients and "Spicules" (marine sponge derivatives) designed to mimic the plumping effect of adipose tissue and stimulate collagen.

- High-Tech Tools: At-home microcurrent and radiofrequency devices marketed specifically to tighten "post-weight-loss" skin.

- Ingestible Beauty: Supplements rich in collagen and protein, catering to the "protein-seeking" behavior of GLP-1 users who need to maintain muscle mass and skin elasticity.

The narrative here is one of "Metabolic Beauty." Consumers now expect their serums and supplements to act as "wellness diagnostics," merging cosmetic benefits with measurable health outcomes. The "Ozempic" user is the prototype for this trend—someone who medically manages their metabolism and expects their beauty routine to support that biological intervention.

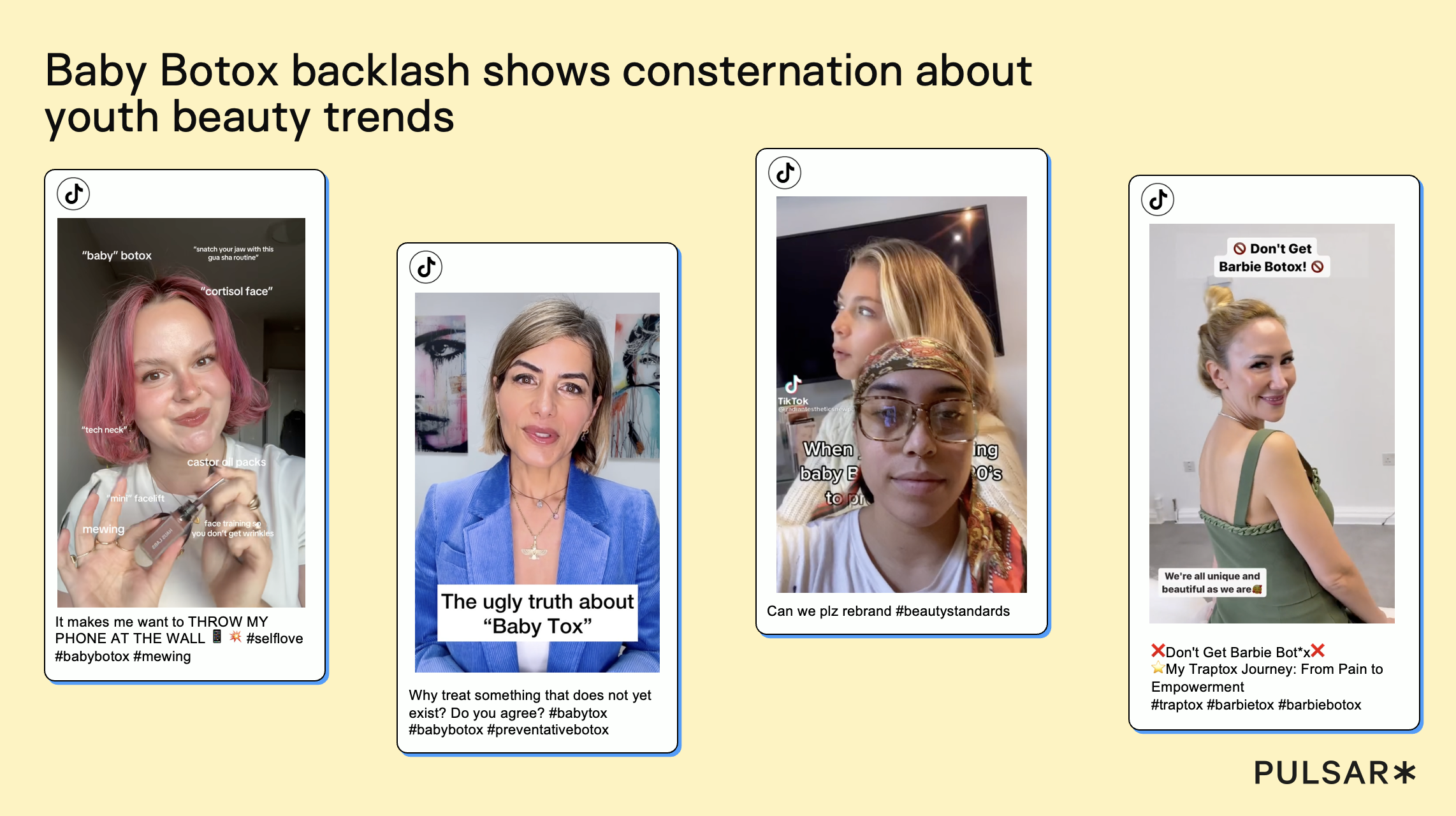

"Baby Botox" and The Prevention Generation

In 2026, preventative injectables such as Baby Botox (#babybotox) and Vampire Facials (#vampirefacial) are emerging as defining beauty trends on social media, shaped by how treatments are named, clustered, and circulated on TikTok. As discussed in The Future of Beauty webinar, injectable-related hashtags function as behavioral signals, revealing how audiences understand and adopt aesthetic treatments in real life. Core terms like #botox and #filler anchor the conversation, while adjacent hashtags including #prp, #medspa, and treatment-specific names connect injectables to skincare, non-surgical procedures, and routine self-maintenance.

View on Threads

Baby Botox refers to low-dose, preventative botulinum toxin injections designed to limit muscle movement early in adulthood, with the aim of reducing visible signs of aging later on. Vampire facials, meanwhile, are PRP (platelet-rich plasma) treatments in which a patient’s blood is processed to concentrate platelets before being re-injected into the skin to support regeneration.

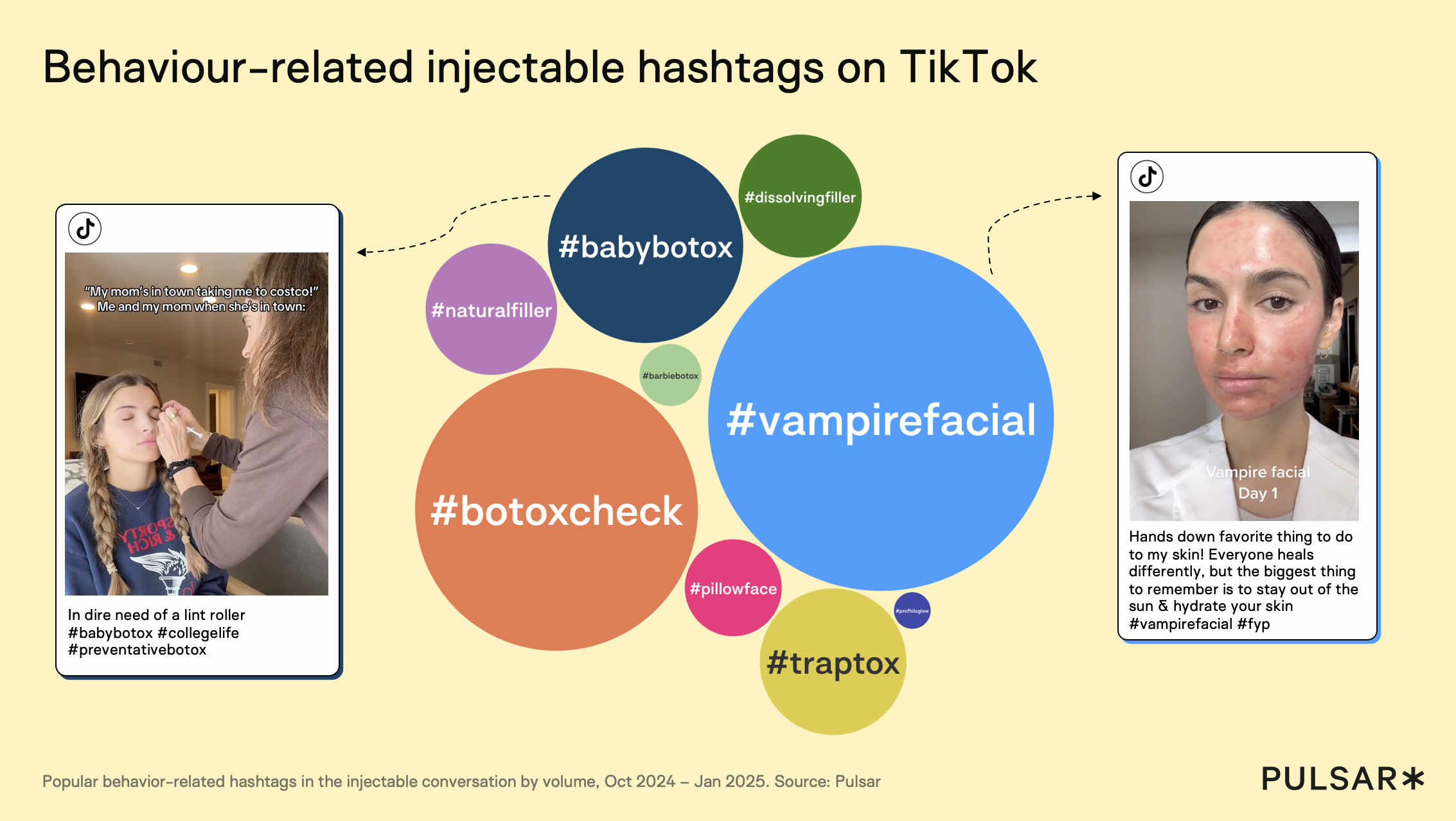

Behavior-related hashtags dominate injectable conversations on TikTok, indicating normalization through routine, not medical framing. #vampirefacial is the most prominent hashtag by volume, outperforming botox-specific terms. #babybotox and #botoxcheck reflect increased peer scrutiny and documentation of cosmetic procedures. Hashtags such as #traptox and #pilloface show the diversification of injectable language into lifestyle and body-specific trends. Injectable discourse on TikTok is organised around personal experience, visibility, and progress tracking, rather than clinical outcomes.

The rise of #vampirefacial demonstrates how language drives adoption: “PRP” conveys medical legitimacy, “facial” implies natural skincare, and “vampire” adds an element of power, danger, and intrigue that fuels virality. #Babybotox, by contrast, reflects a preventative framing of injectables, positioned as early intervention rather than anti-aging correction.

View on Threads

The age of entry for injectables continues to plummet. "Baby Botox"—micro-doses of neurotoxins used preventatively—is a dominant topic in social commentary. The narrative has shifted from "reversing time" (reactive) to "stopping time" (preventative). Data from the aesthetic medicine market projects that non-surgical treatments will continue to outpace surgical ones, with the global non-invasive market valued at over $21 billion and growing. The 2026 consumer, particularly those in the 25-34 demographic, views these treatments as "future-proofing." They are not looking for the frozen look of the 2010s; they are looking for "high-functioning skin."

Social media conversations increasingly frame “baby botox” as controversial rather than aspirational, with visible pushback against preventative injectables. Content criticizing baby botox focuses on youth pressure, unrealistic beauty standards, and unnecessary medicalisation of aging. TikTok creators explicitly challenge the idea of treating wrinkles “before they exist,” signaling a shift from normalization to resistance. Counter-narratives emphasize self-acceptance and empowerment, positioning rejection of injectables as an act of agency. The backlash is driven by peer-to-peer creator content, not traditional media or brands.

Its youthful, softened language mirrors broader trends in beauty marketing, where treatments are branded earlier, sweeter, and more casually, even as backlash and concern begin to surface. Together, these conversations show how injectables in 2026 are trending as socially normalized beauty behaviors, shaped as much by platform culture and influencer storytelling as by clinical outcomes.

3. The Evolution of Natural Deodorant: The Compromise Economy

The natural deodorant category offers a fascinating case study in the 2026 consumer's willingness to engage in "The Compromise Economy". A Pulsar TRAC analysis, in collaboration with cultural foresight consultancy Sign Salad, uncovers a profound shift in the semiotics of personal care.

Semiotics of Sweat: From Suppression to Acceptance

Historically (since the 1950s), deodorant marketing relied on a binary narrative: "Wetness is bad; Dryness is good." Visual cues were clinical (shields, arrows blocking sweat) or gender-stereotyped (daisies for women, competitive sports for men).15 The goal was total suppression of biological function.

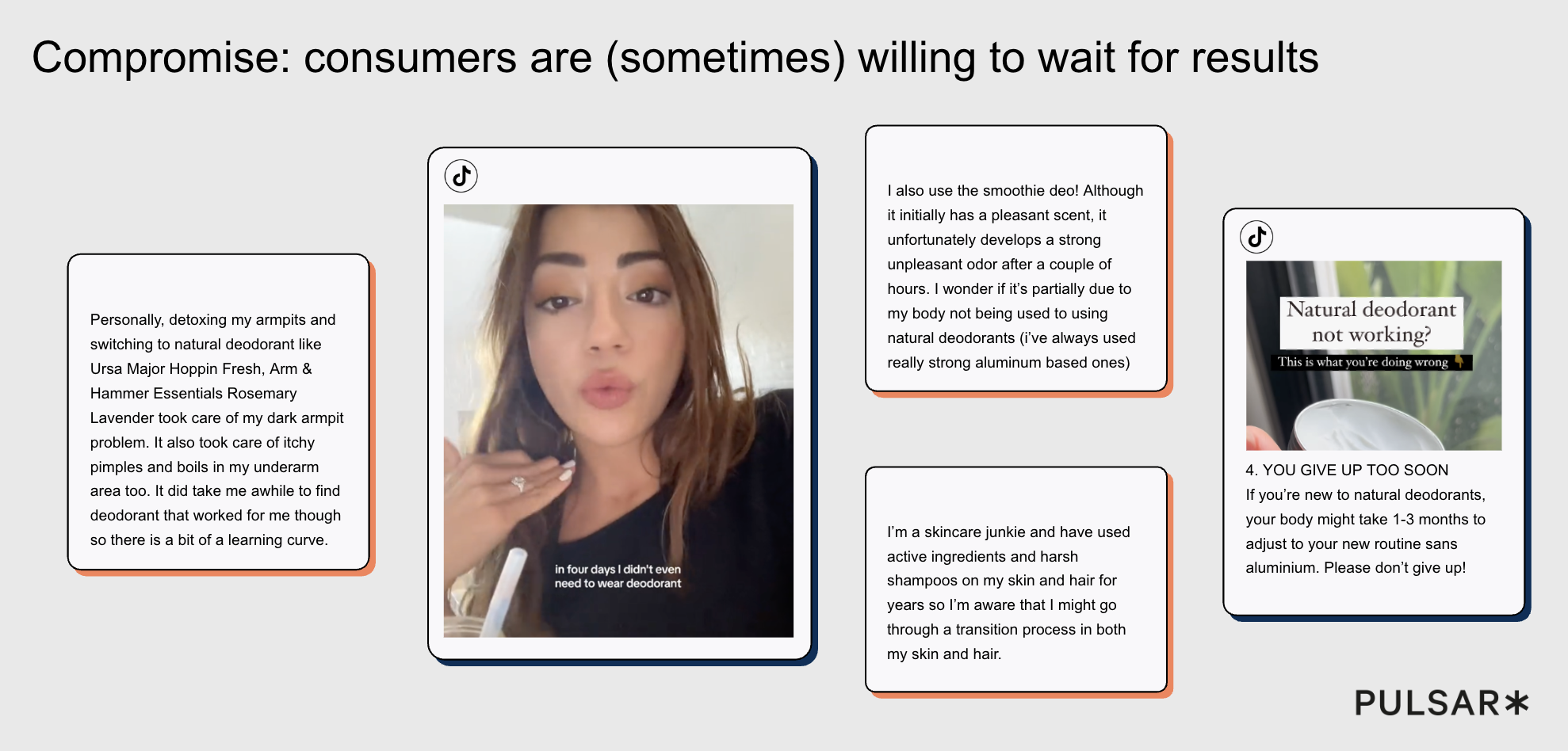

Consumers increasingly accept delayed efficacy in beauty routines when outcomes are framed as healthier or more natural. Natural deodorant conversations emphasize adjustment periods, detox phases, and learning curves. Peer advice frequently reassures audiences that results may take weeks or months, reframing inconvenience as commitment. TikTok and forums content position patience as a virtue and marker of informed consumption. Temporary discomfort or inconsistency is normalized as part of long-term behavioral change, not product failure.

By 2026, the "Natural Deodorant" category has disrupted this semiotic landscape. It has moved from a functional product to a "semiotic playground". The new narrative is not about blocking biological functions (which is now seen as "unhealthy" or "toxic" by the wellness-conscious consumer) but about managing them with "clean" ingredients. Brands are using experimental, playful, and gender-neutral visual codes to signal this shift.

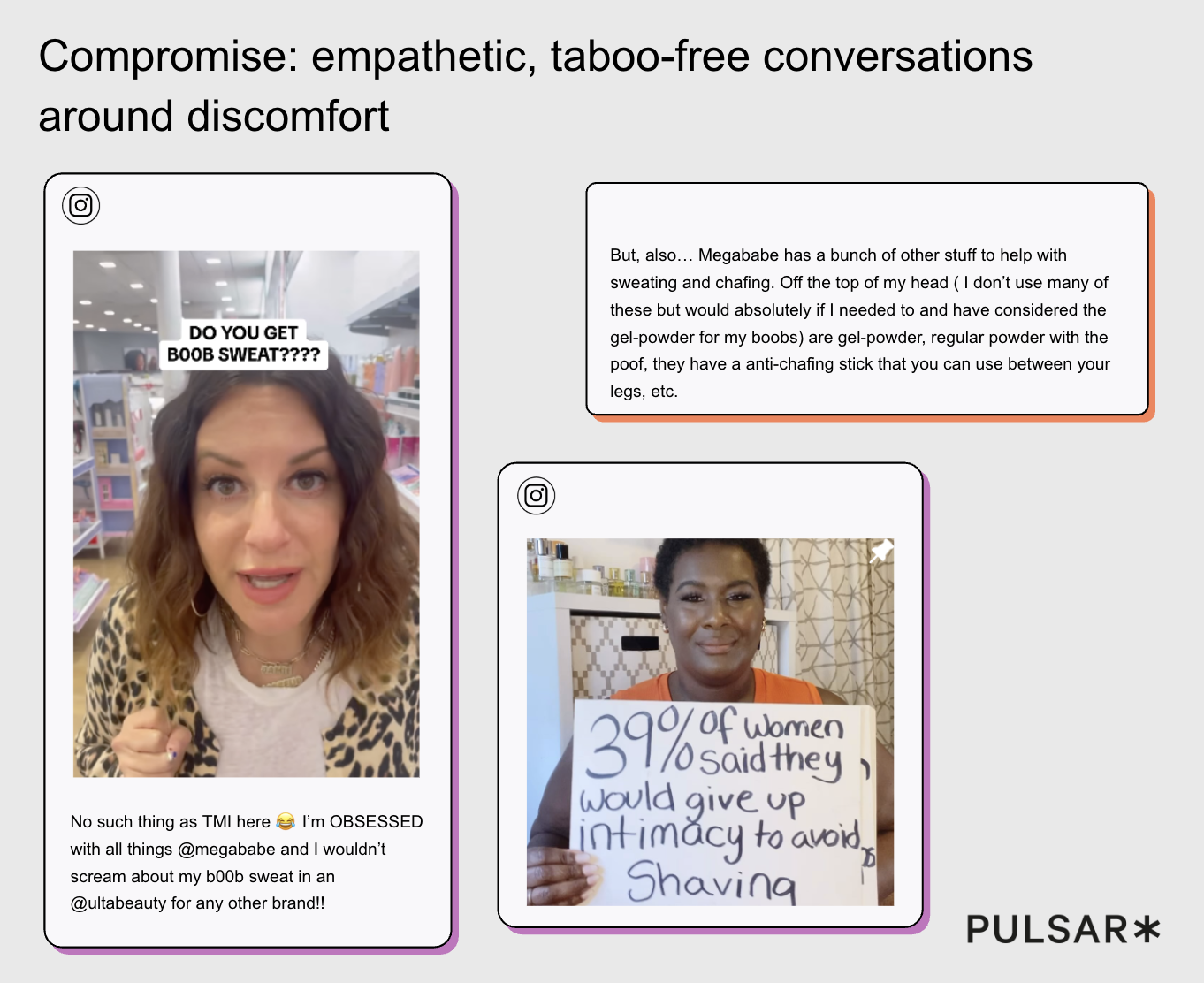

Beauty conversations increasingly normalize previously taboo bodily discomforts, including sweat, chafing, shaving, and intimacy-related concerns. Social content frames discomfort through empathetic, peer-led language, reducing stigma rather than promising transformation. Brands such as Megababe are referenced in the context of practical problem-solving, not aspiration or perfection. Audience engagement is driven by relatability and openness, with creators explicitly rejecting “TMI” boundaries. Beauty discourse is shifting from aesthetic outcomes toward care, comfort, and bodily honesty.

However, this shift requires a consumer compromise. Natural deodorants often lack the antiperspirant efficacy of aluminum-based competitors. The Pulsar/Sign Salad analysis reveals that consumers are actively discussing this "sacrifice". They are trading "convenience" (staying dry for 48 hours) for "values" (health anxiety, sustainability, aluminum-free status).

The natural deodorant vs. stink debate is valid but I also don’t want cancer and rubbing chemicals on ur lymph nodes every day is awful. SO, with that said, I use this deodorant which is better than alternatives and I literally never stink. I’m sure it’s still not the best or pic.twitter.com/BpNibLRbeT

— 𝚃𝚑𝚒𝚌𝚌 𝙲𝚑𝚞𝚗𝚐𝚞𝚜 🍄 (@anactualwalnut) July 24, 2023

This trend extends beyond deodorant into a broader "Compromise vs. Efficacy" debate in 2026. Whether it is sustainable packaging that dissolves too quickly or "clean" mascara that smudges, consumers are constantly weighing moral satisfaction against performance. The "Compromise Economy" is defined by consumers who knowingly choose a less effective product because it aligns with their identity as an "ethical consumer."

Consumer Motivations in the "Compromise Economy":

- Health Anxiety: Fear of aluminum and "toxins" drives the switch, even if it means sweating more.

- Sustainability: Desire for plastic-free or refillable packaging (e.g., cardboard tubes) despite functionality issues.

- Identity Signaling: Using natural deodorant is a "badge" of being "in the know" about wellness trends.

The Return of Efficacy: "Science-Backed Natural"

Interestingly, 2026 is also seeing a counter-trend: a demand for "Science-Backed Natural." Consumers are fatigued by "clean washing" and products that fail to perform. The rise of ingredients like Kanuka oil (the "new Manuka")—touted as antibacterial and anti-inflammatory—suggests a push to close the efficacy gap. The "Metabolic Beauty" trend reinforces this: if a product is "healthy," it must also be "high-performance."

Strategic Implication: Brands in the "natural" space can no longer rely on fear-mongering about "toxins" alone. They must prove efficacy. The 2026 marketing narrative is: "Works as hard as chemicals, without the compromise." We will see a rise in "hybrid" products that use biotechnology to mimic the efficacy of synthetic ingredients without the perceived "toxicity."

4. Acne Acceptance: Starface, The "Cute-ification" of Flaws, and Performative Vulnerability

If there is one brand that defines the Gen Z/Alpha approach to beauty in 2026, it is Starface. Their trajectory from a niche startup to a "mainstream cultural object" illustrates a fundamental rewriting of the rules of skin conditions.

From Stigma to Statement Accessory

The Pulsar analysis highlights a "significant cultural shift" where acne has moved from "social downfall" to "statement accessory". Starface's yellow "Hydro-Stars" did not just treat acne; they framed it. By turning a pimple patch into a bright, collectible sticker, they gamified the breakout.

In 2026, this trend has matured. Pimple patches are now a "collective category" and a "fashion-cultural object". They appear on high-fashion runways (e.g., Ashley Williams SS26) and on celebrities, signaling an "effortlessly cool blasé attitude". The patch is a "badge" that says, "I am human, I have skin, and I don't care if you see it." This is Performative Vulnerability, the act of publicly displaying a flaw to accrue social capital.

The chair earrings from Ashley Williams ss26 are so unserious. I love them. pic.twitter.com/WQq98QN83A

— andrianaシ (@BOTTEGAHOENETA) October 11, 2025

The Fragmentation of the Patch Market

Starface's success has, ironically, led to a decline in its share of the conversation as the market fragments. The category has exploded with competitors, creating a tiered market:

- The Aesthetic Tier (Starface): Focus on "cute-ification," collectibility, and collaborations (Hello Kitty, SpongeBob). This tier dominates on "slower-burn" community spaces like blogs and forums where brand loyalty is deep.

- The Clinical Tier (Hero Cosmetics, ZitSticka): Focus on "invisible" or "medical-grade" efficacy for those who want the function without the fashion.

- The Dupe Tier: Low-cost knockoffs flooding platforms like TikTok Shop and Temu.

Starface no longer dominates the pimple patch conversation, despite being an early category leader. Mentions of “pimple patches” as a category consistently outweigh mentions of Starface, indicating category growth beyond a single brand. Over time, Starface’s share of conversation fluctuates independently of overall category interest, suggesting rising competition. Peaks in pimple patch discussion are not matched by proportional increases in Starface mentions, signaling brand dilution within a growing market. The data shows a shift from brand-led discovery to category-led behavior, where consumers discuss the product type rather than a flagship brand.

The "Cute-ification" of Medical Conditions

This trend has bled into the wider industry. We are seeing the "cute-ification" of all "problem/solution" categories. Eczema creams, cold sore treatments, and even period products are adopting the "Starface aesthetic"—bold colors, ironic voice, and sticker-ability. It is a rejection of the sterile, clinical beige of traditional dermatology.

djed wearing starface pimple patches and matching them with the kit is actually the cutest thing ever 😭🥹 pic.twitter.com/LIcSmeE2uk

— kayla ⁷ (@k_son7) January 12, 2025

Strategic Implication: The lesson of Starface is that Visibility > Invisibility. For Gen Z, hiding a flaw implies shame. Decorating a flaw implies power. Brands addressing "negative" conditions (dandruff, bloating, scarring) should explore "loud" branding rather than "discreet" solutions. The 2026 consumer wants to "wear" their wellness journey.

5. Dupe Culture: The "Doop" Economy and the Death of Brand Loyalty

"Dupe Culture" has evolved from a fringe money-saving tactic to a central pillar of the 2026 beauty economy. It is no longer about "settling" for less; it is about the thrill of the hunt, the signaling of financial literacy, and the democratization of luxury. In beauty specifically, this is playing out through viral moments around skincare, makeup and fragrance dupes, from affordable alternatives to prestige serums and foundations, to mass-market fragrances positioned as replicas of luxury scents.

Pulsar’s analysis of 850,000 conversational data points reveals that the "Dupe" conversation is driven by a complex mix of economic and social factors. Beauty creators on TikTok and Instagram increasingly frame dupes as “formula matches” or “ingredient twins,” reinforcing the idea that performance, not brand, is what matters.

- Financial Pressure: The rising cost of living makes affordability a necessity.

- Insider Status: Finding a dupe feels like "hacking the system." It creates a sense of being an "insider to an anarchic viral trend." In beauty, this insider status is often earned by identifying the exact active ingredients, textures or undertones that make a dupe comparable to a cult product.

- Visual Validation: Engagement is highest on posts that visually compare the "Dupe" vs. the "Original" side-by-side.24 These images are "proof of work"—evidence that the cheaper product performs equally well. Side-by-side swatches of complexion products, wear tests of mascaras, and texture comparisons of serums have become core formats in beauty dupe content.

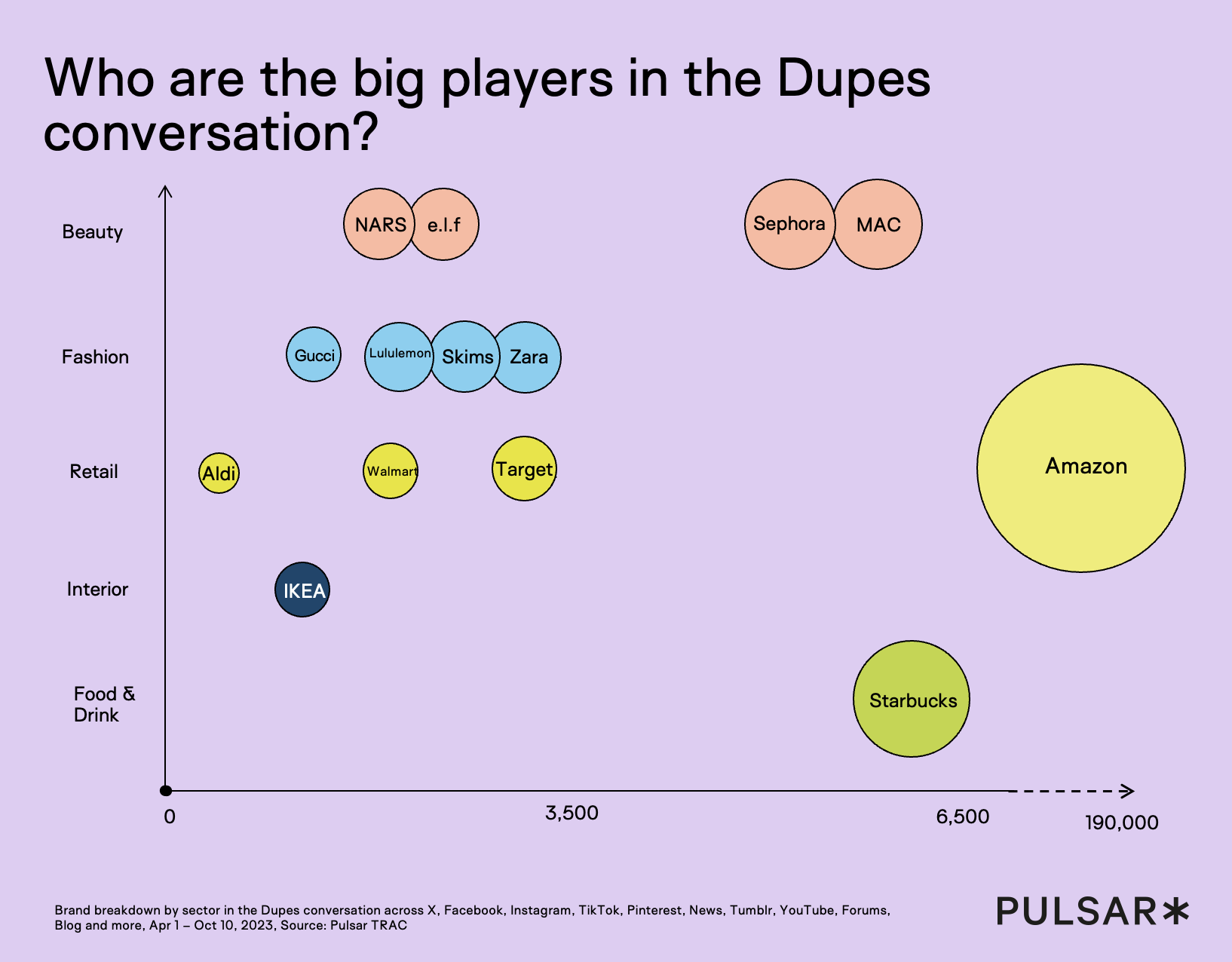

Amazon overwhelmingly dominates the dupes conversation, generating approximately 190,000 mentions, far surpassing all other brands. Starbucks is the second most visible brand, with around 65,000 mentions, highlighting dupes extending beyond beauty into food and drink. In beauty retail, Sephora and MAC cluster around roughly 3,500 mentions each, indicating moderate but meaningful presence. Beauty-specific dupe moments often reference affordable brands positioned against prestige players, with mass-market skincare, makeup and fragrance brands repeatedly surfaced as alternatives to luxury launches. Retailers such as Target, Walmart and Aldi play a visible role, reinforcing the association between dupes and accessible retail. The spread of brands across beauty, fashion, retail, interiors and food & drink shows dupes functioning as a cross-category consumer behavior, not a single-sector trend.

The Symbiosis of Luxury and Dupe

Contrary to fears that dupes would destroy luxury, the relationship has become symbiotic. Viral dupe trends often increase brand awareness for the original product (the "Duped"). In beauty, luxury launches frequently act as the spark that ignites a wave of dupe content, with creators explicitly naming the prestige product as the benchmark. For the 2026 consumer, owning the luxury item is a flex of wealth, but owning the dupe is a flex of intelligence.

However, this creates a Loyalty Crisis. Data suggests 57% of Gen Z are "less brand loyal" than before. They shop by molecule and performance, not by logo. This is particularly pronounced in skincare and complexion makeup, where ingredient lists, claims and efficacy are easily compared. If a $10 serum has the same active ingredients as a $100 serum, the brand equity of the luxury player evaporates unless they can offer something intangible (packaging, scent, status).

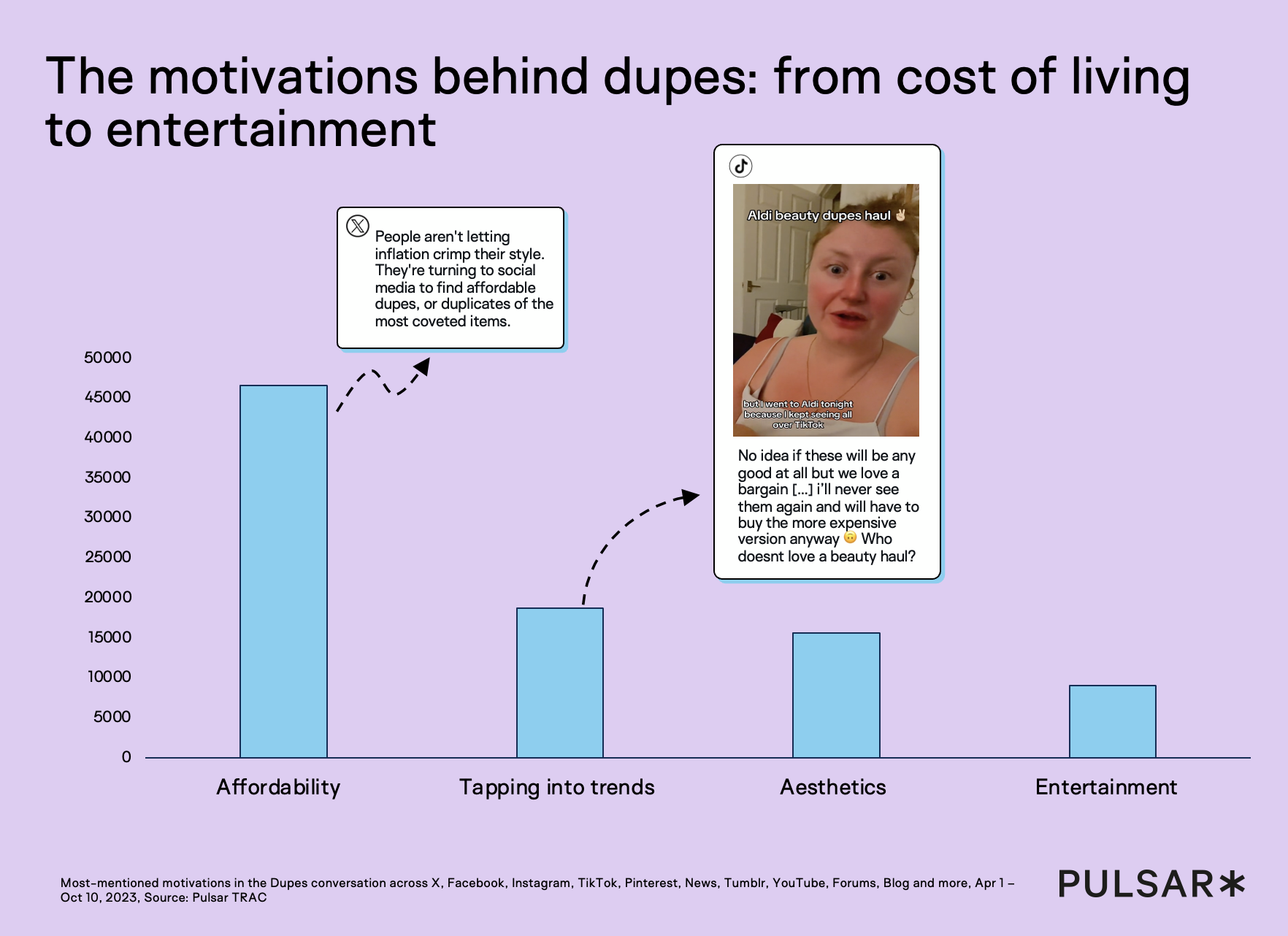

Affordability is the dominant motivation in dupe conversations, driving around 45,000 mentions, far exceeding all other drivers. Mentions of dupes motivated by tapping into trends reach roughly 18,000, showing that trend participation remains a secondary but significant driver. Aesthetic similarity accounts for approximately 15,000 mentions, indicating that visual resemblance matters less than price. Entertainment-driven dupe content is comparatively niche, with under 10,000 mentions, despite strong visibility on TikTok. In beauty, this entertainment layer often takes the form of “full face of dupes” videos or long-wear tests that turn product comparison into spectacle. The data shows dupe culture evolving from cost-of-living necessity to content-driven entertainment, without entertainment overtaking affordability as the primary driver.

The "Dupe" as a Path-to-Purchase

The impact on shopping behavior is material. Consumers now "audit" products in-store, using visual search and TikTok to check for dupes before purchasing. This behavior is especially visible in beauty aisles, where shoppers compare shades, textures and ingredient lists in real time. The "Dupe" is a standard step in the path-to-purchase funnel. We are also seeing the rise of "Dupe-Proof" marketing—brands emphasizing proprietary technology (e.g., patented molecules, unique delivery systems) that literally cannot be duped by a generic lab.

Strategic Implication: Brands have two choices:

- Embrace the Dupe: Create "official dupes" or "entry-level" versions of hero products to capture the price-conscious consumer. Beauty brands are increasingly experimenting with mini sizes, simplified formulas or diffusion lines to intercept dupe-seeking audiences.

- Dupe-Proof the Brand: Invest heavily in "Sensorial Synergy" and "Emotional Storytelling". A scent, a texture, or a brand vibe is harder to copy than an ingredient list. The "Metabolic Beauty" trend aids this—proprietary biological data cannot be "duped."

What Beauty Brands Can Learn From This

As we survey the landscape of 2026, the overarching theme is Resilience. The consumer is building a "resilient" face (via preventative Botox and metabolic skincare) to weather the aging process. They are building a "resilient" wallet (via Dupe culture) to weather economic instability. And they are building a "resilient" identity (via Glitchy Glam and Acne Acceptance) to weather the pressure of AI perfection.

The "Great Fragmentation" has made the job of the beauty strategist infinitely harder. There is no single "consumer" to target. There is the Bio-Purist who fears AI and demands clean deodorant; the Techno-Optimist who uses AI to track their skin metabolism; the Glitchy Glam rebel who wears mismatched eyeshadow; and the Metabolic Maximizer who views beauty as a medical discipline.

Key Strategic Beauty Takeaways for 2026

AI in Beauty

- The shift: Novelty → Uncanny Valley anxiety

- What’s changing: As AI-generated imagery and tools become commonplace, audience excitement is increasingly tempered by discomfort around realism, authenticity, and mental well-being.

- Strategic action: Pivot towards a human-first AI approach. Use technology to enhance real faces and bodies rather than replace them, and articulate clear brand values around transparency, mental health, and responsible AI use.

Injectables and Preventative Aesthetics

- The shift: Correction → Ongoing maintenance

- What’s changing: Conversations around injectables move away from dramatic transformation towards preventative, routine-led interventions like baby botox and PRP-based treatments.

- Strategic action: Develop peri-procedure skincare and aftercare lines that focus on regeneration and recovery, leaning into narratives around skin longevity, repair, and optimization rather than anti-ageing.

Natural Deodorant

- The shift: “Clean” → Compromise

- What’s changing: Audiences openly acknowledge the trade-off between natural formulations and performance, reframing natural deodorant as a negotiated choice rather than a perfect solution.

- Strategic action: Emphasize science-backed natural innovation. Communicate clearly how new formulations close the efficacy gap, rather than relying on purity-led claims alone.

Acne Acceptance

- The shift: Conceal → Decorate

- What’s changing: Social content increasingly reframes acne from a flaw to be hidden into something visible, playful, and styled, driven by creator culture and self-expression.

- Strategic action: Gamify imperfection. Create products and packaging that turn skin concerns into expressive features, following the logic of “cute”, collectible, and identity-led design.

Dupe Culture

- The shift: Knockoff → Lifestyle choice

- What’s changing: Dupes are no longer framed as inferior substitutes, but as smart, values-led decisions tied to affordability, access, and cultural savvy.

- Strategic action: Luxury brands should double down on experience, heritage, and proprietary technology. Mass brands should confidently embrace the “smart shopper” narrative and position dupes as intentional, informed choices.

Looking Forward to 2026

Looking to 2026, the defining characteristic of beauty trends on social media is not consensus, but choice. Audiences are actively navigating competing narratives around technology, aesthetics, health, and authenticity, selecting what aligns with their values rather than passively adopting dominant looks. AI is embedded across the beauty ecosystem, but increasingly contested. Injectables are normalized as lifestyle maintenance, yet subject to scrutiny. Imperfection is visible and styled, while brand loyalty is weakened by dupe culture and performance-led comparison.

For beauty brands, success in 2026 depends on understanding beauty trends as cultural behaviors rather than product moments. The brands that perform best will be those that read audience narratives early, anticipate backlash as well as adoption, and communicate with clarity and restraint. In an environment where beauty trends emerge from social platforms faster than marketing cycles can respond, audience intelligence becomes a strategic necessity. The future of beauty on social media will belong to brands that can navigate complexity, earn trust, and remain culturally fluent as beauty continues to fragment, accelerate, and reassemble in public view.

To stay up to date with our latest insights and releases, sign up to our newsletter below: