Social Listening for the Finance Sector: A Practical Guide to Audience and Narrative Intelligence

The financial services landscape in 2025 is no longer defined solely by balance sheets and interest rates but by the volatile flow of digital narratives and the complex psychographics of global audiences. As traditional institutions grapple with a systemic crisis of trust and the rapid ascent of decentralized alternatives, the necessity for sophisticated intelligence has moved beyond simple social media monitoring. For the modern financial brand, survival and growth depend on the ability to transition from reactive listening to a proactive model of narrative intelligence. This discipline involves not only tracking what is being said but mapping the underlying cultural currents, identifying the specific communities driving these conversations, and activating insights to bridge the gap between institutional goals and consumer expectations.

The current economic climate is characterized by what has been termed a "crisis of grievance," where institutional failures over the past two decades have fostered deep-seated resentment across various demographics. This grievance is particularly potent in the financial sector, where perceptions of inequality, fears of misinformation, and the devaluation of fiat currency have led to an intensifying anxiety regarding the future of the global economic order. In this environment, social listening serves as an essential sensory organ, allowing brands to detect the early signals of reputation risk and the subtle shifts in consumer behavior that traditional market research often misses.

Contents

- Audience Intelligence for Finance: Moving Beyond Demographics

- Social Listening for Brand Reputation Crisis in Finance

- The Evolution of Credit: Buy Now, Pay Later (BNPL)

- Alternative Currencies and the Distrust of Fiat

- AI and the Future of Financial Experience

- The Framework of Intelligence: Listen, Map, and Activate

- Conclusion: Why Social Listening Is Now Essential for Finance Brands

Audience Intelligence for Finance: Moving Beyond Demographics

A persistent challenge in financial marketing is the over-reliance on demographic data, which often results in low engagement rates and missed opportunities. Demographic segmentation—dividing audiences by age, gender, income, or location—provides only a superficial understanding of a consumer. In contrast, audience intelligence delves into psychographics, which describe the motivations, attitudes, values, and specific behaviors that drive financial decision-making.

Psychographic Profiling in the Financial Sector

The limitations of demographics are particularly evident when considering a broad cohort such as "women aged 25–54 with incomes between $25,000 and $50,000". This group does not share identical values or financial needs; some may be "Explorers" who are the first to try new fintech apps, while others may be highly risk-averse and suspicious of digital-only solutions. Audience intelligence allows marketers to move away from these sweeping judgments and connect with consumers in more meaningful ways.

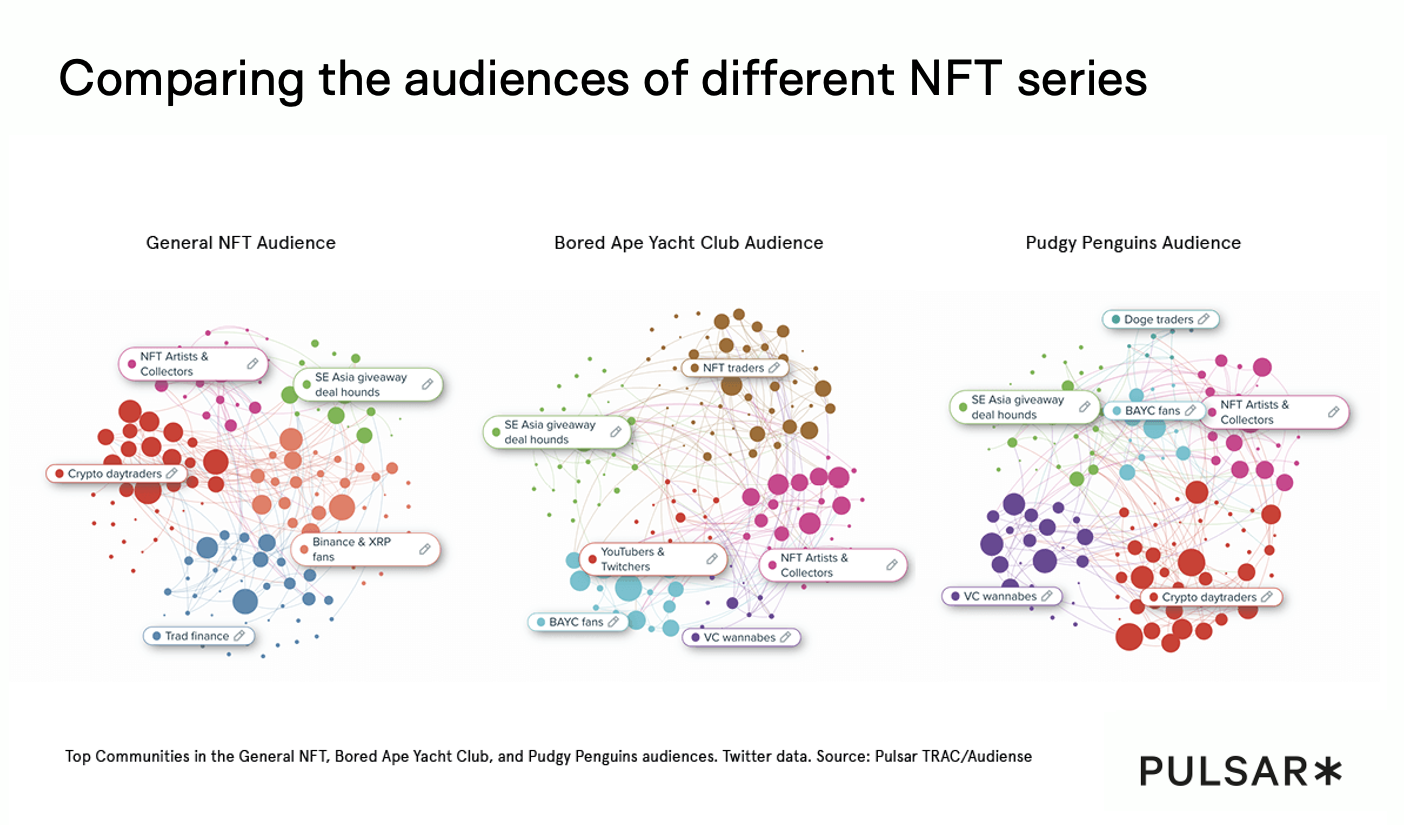

For example, when we examined the audience for NFT brands like Bored Ape Yacht Club (BAYC) or Pudgy Penguins, we identified distinct sub-communities such as "Wannabe VCs" (aged 25–34 with high affinity for Silicon Valley figures) and "SE Asia Giveaway Deal Hounds". Each of these groups requires a different messaging strategy: the "Wannabe VCs" might respond to technical roadmap updates, while the "Deal Hounds" are motivated by rewards and entry-level accessibility.

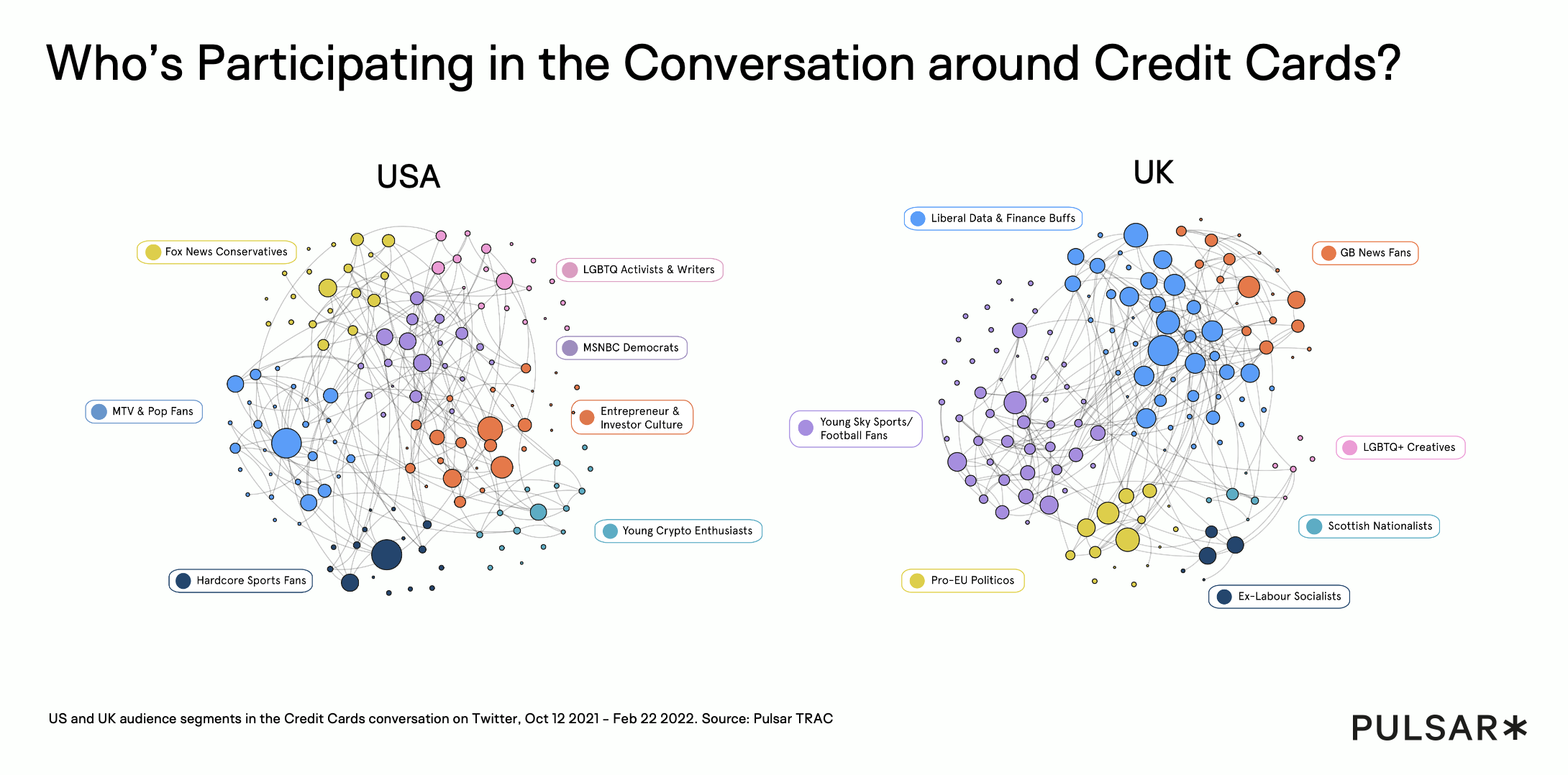

Transactions and Reactions in the Credit Card Conversation

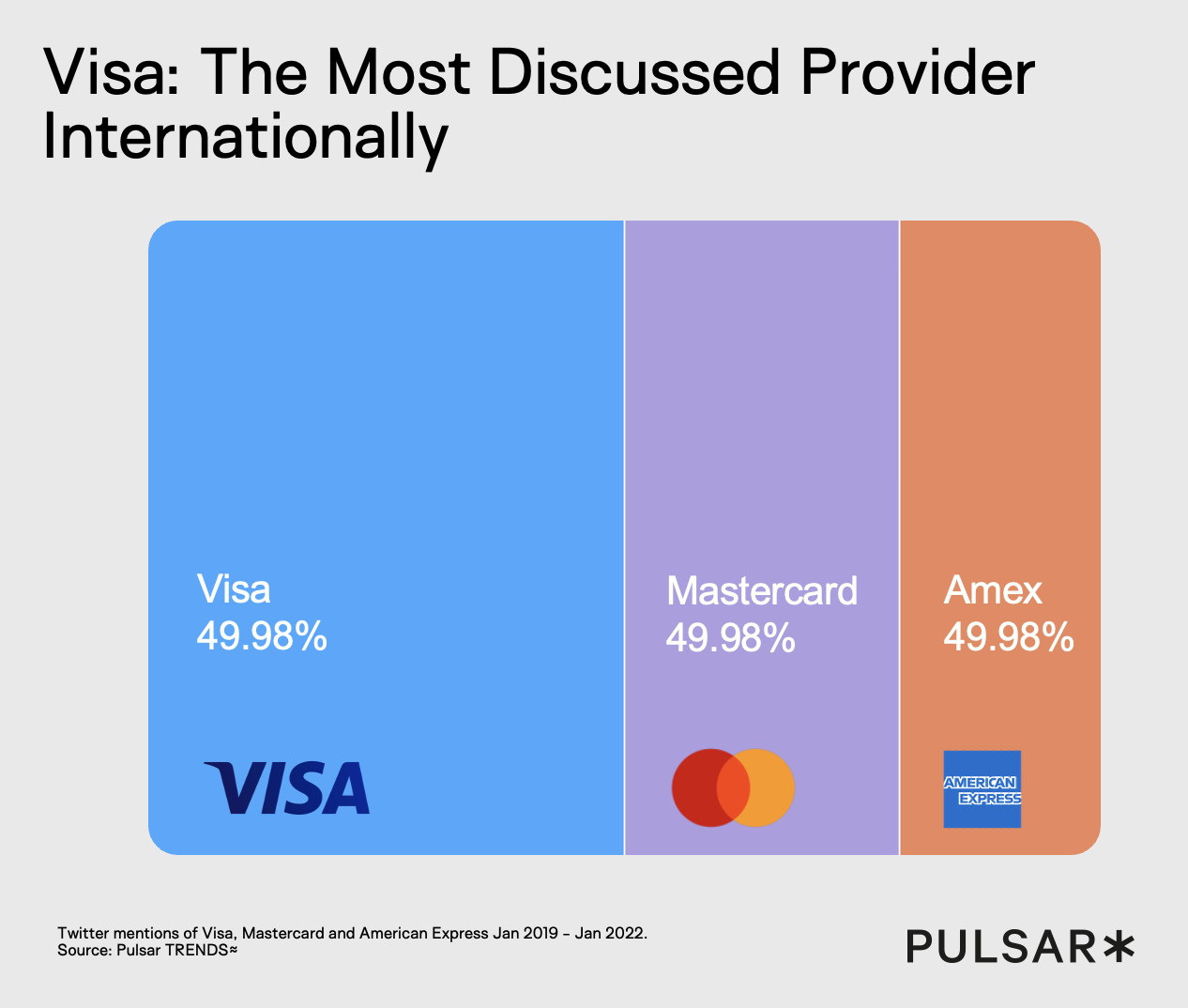

Here at Pulsar we examined the global credit card conversation. In our analysis of more than half a million English-language posts from social media, forums, blogs and review sites, the global credit-card conversation reveals distinct patterns of engagement and meaning that extend far beyond simple transaction mechanics. Credit cards such as Visa, Mastercard and American Express no longer function solely as instruments of payment; they have become cultural touchpoints embedded within the lives and values of diverse online communities.

Across this conversation, audience segments differ markedly in both cultural orientation and topical focus. Traditional finance topics coexist with discussions that link cards to broader social and lifestyle themes, while community clusters such as *MTV & Pop Fans* engage with cards in the context of sponsored events or entertainment whereas *Young Crypto Enthusiasts* foreground technological innovation, speculation and rewards in the context of blockchain ecosystems.

This so-called nascent generation—particularly evident among younger, tech-savvy cohorts—frames credit cards through lenses that contrast sharply with earlier cohorts. For these users, discussions often emphasize innovative integrations (such as crypto-linked rewards and blockchain-oriented platforms) rather than traditional banking relationships. Their participation in the credit card conversation blends financial behaviour with expressions of identity and community affiliation; they articulate views about these products not only as financial tools but as enablers of new modes of value exchange and participation in decentralized economies.

Social Listening for Brand Reputation Crisis in Finance

In the hyper-connected financial world, a narrative can escalate from a niche forum post to a full-blown bank run or reputation crisis in a matter of hours. The Silicon Valley Bank (SVB) crisis and the "Brand Misinformation" risks faced by J.P. Morgan and American Express serve as cautionary tales of how unmanaged narratives can threaten institutional stability.

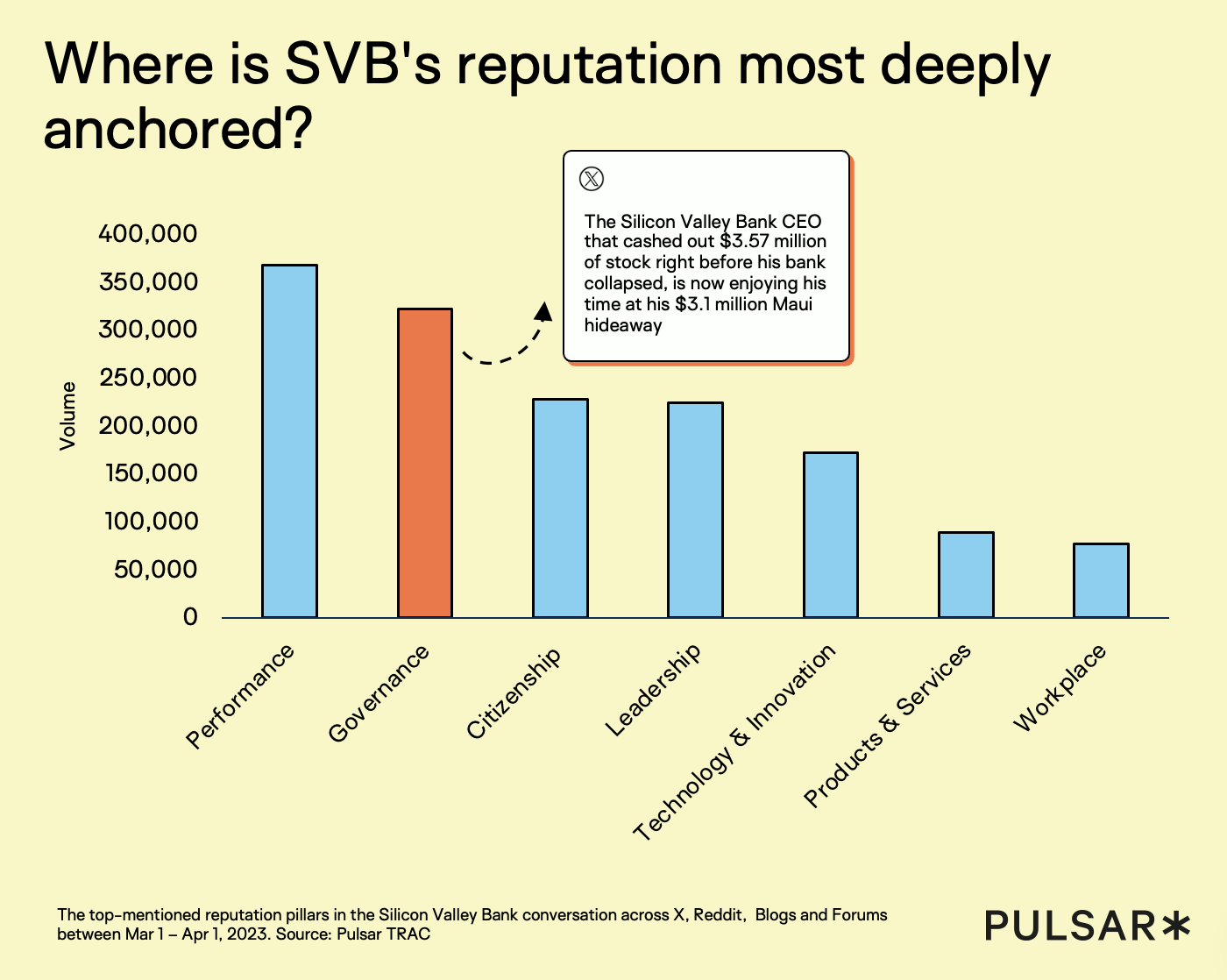

The SVB Crisis: A Contagion of Distrust

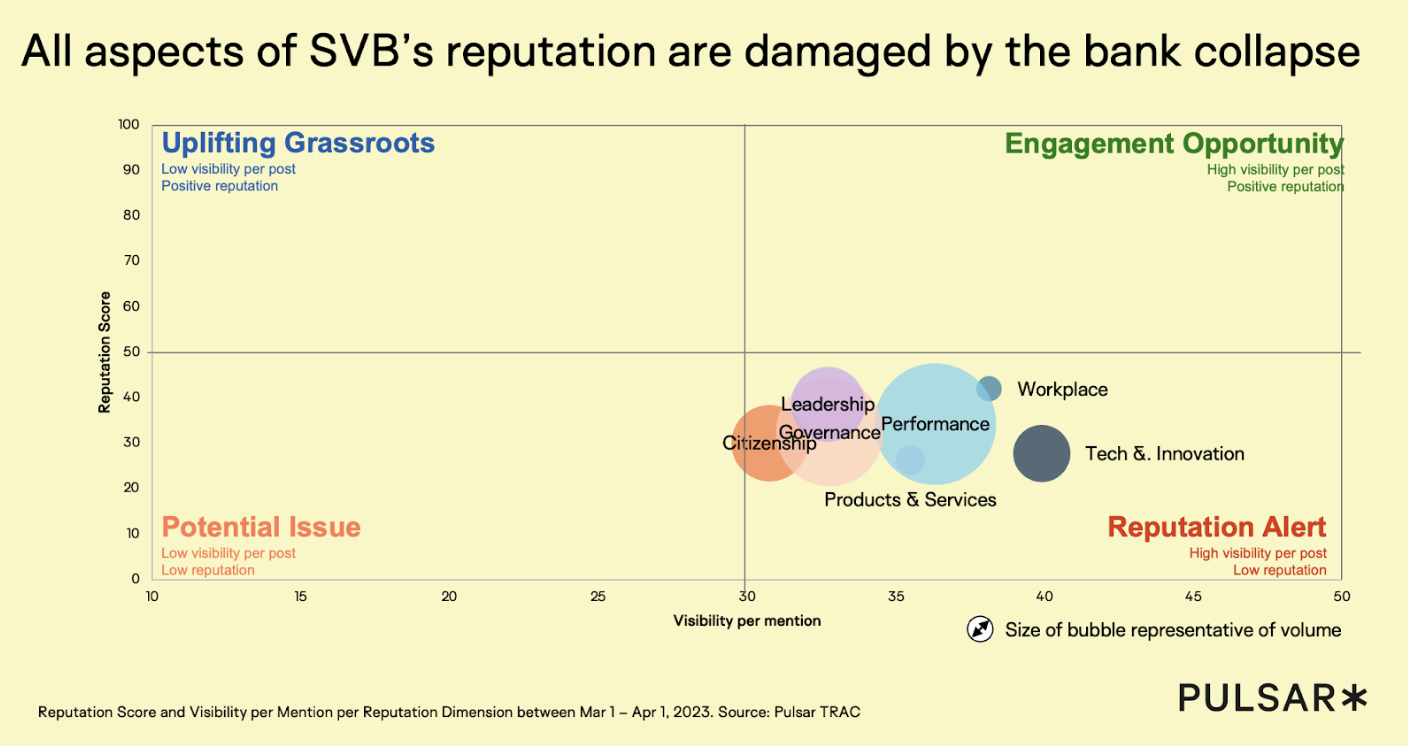

Our analysis of the Silicon Valley Bank collapse shows that financial brand crises are driven by rapid shifts in reputational narratives rather than sustained conversation volume. The SVB brand reputation crisis was not a singular event but a convergence of narratives framed by different political and social communities. As the crisis unfolded, discussion concentrated on key reputation pillars—particularly performance, governance, leadership, and citizenship—each contributing to a sharp deterioration in brand perception.

Early conversation focused on operational performance and executive decision-making, with scrutiny intensifying immediately after the bank’s closure. As visibility increased, reputation scores fell sharply, indicating escalating reputational damage rather than short-term attention spikes . Over time, narratives expanded into broader debates about ethics, accountability, and regulation, signalling deeper trust erosion.

Audience intelligence reveals that this escalation was uneven. Financial and tech-focused communities drove early analysis, while political and current-affairs audiences later amplified the crisis through high-engagement narratives, accelerating reputational impact despite lower posting volume.

Even as conversation volumes stabilised following external interventions, reputation scores remained below neutral, demonstrating that reputational recovery lagged behind attention. The SVB case highlights why finance teams must monitor reputation pillars, audience shifts, and visibility together to detect when a crisis is evolving into long-term trust damage. Narrative intelligence allows a brand to see these frames as they develop. For financial institutions, the lesson is that a crisis is rarely just about the numbers; it is about the story people tell themselves about those numbers.

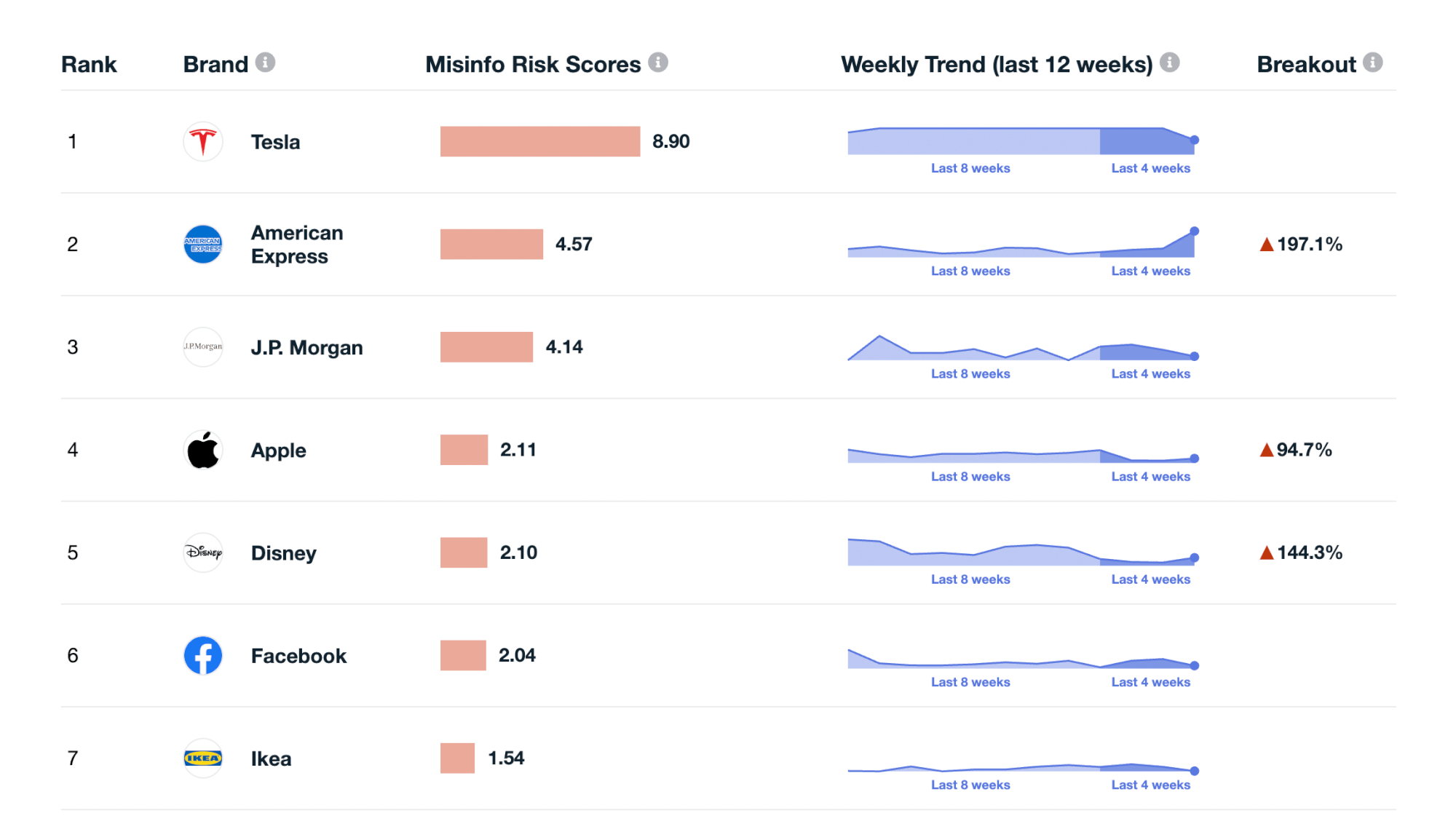

Misinformation Risk: The Rise of Anti-Woke Narratives

Using Pulsar’s partnership with NewsGuard data, we examined misinformation risk in our Misinformation Risk Index. Financial giants like J.P. Morgan and American Express have increasingly found themselves at the center of polarized narratives, such as the "woke cartel" backlash. This narrative, often amplified by high-profile figures like the founder of Tesla, targeted companies on the S&P 500's ESG (Environmental, Social, and Governance) Index. A specific point of contention involved the categorization of gun sales, which certain communities framed as an infringement on constitutional rights by financial intermediaries.

When these narratives gain traction on "untrustworthy news sites" or within specific echo chambers, they create a "misinformation risk" that can lead to boycotts or stock price volatility. Narrative intelligence enables brands to identify the "dimensions of their obligation" to the issue at hand. Silence is often not a safe play, as it can be interpreted as an admission of guilt or a lack of leadership. Instead, brands must map where they have a "license to act" and communicate their values in a way that addresses the root "grievance" of the audience.

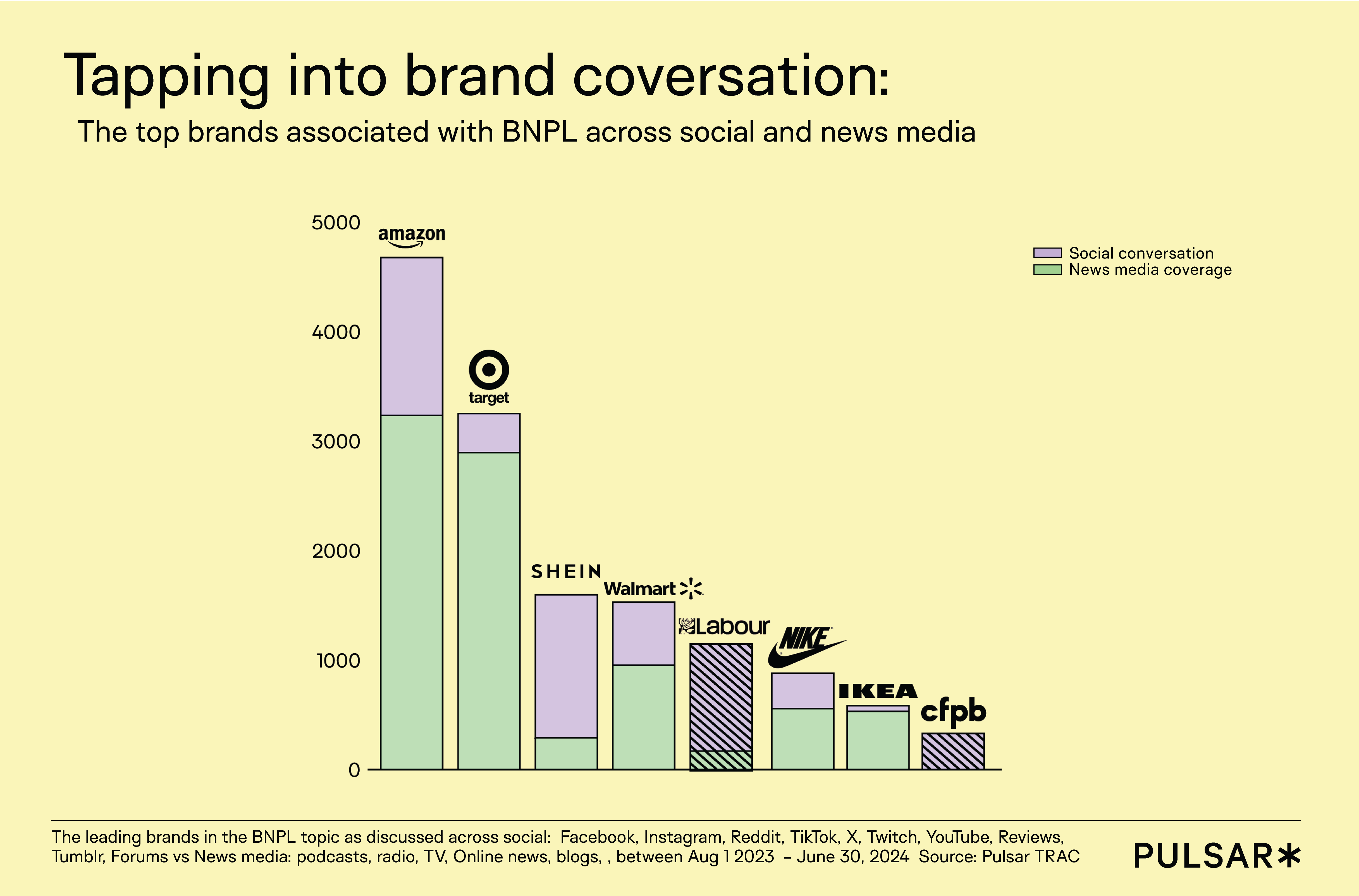

The Evolution of Credit: Buy Now, Pay Later (BNPL)

The Buy Now, Pay Later sector provides perhaps the most striking example of how a narrative can shift from "luxury" to "lifeline" in response to economic pressure. Originally perceived as a trendy tool for Gen Z consumers to buy fashion and beauty products, BNPL has evolved into a crucial mechanism for purchasing necessities like groceries, utilities, and auto repairs.

The Shift from Luxury to Survival

In 2024 and 2025, our research into the BNPL conversation moved from "spending for pleasure" to "spending for survival". This shift is particularly pronounced in regions like Australia and the UK, where the cost-of-living crisis has forced consumers to look for alternative credit options. In Australia, consumers have expressed concern about using BNPL for essentials like petrol, while in the US, the narrative has been shaped by the integration of services like Apple Pay Later and Affirm into mainstream retail platforms like Amazon.

This transition has given rise to the narrative of "phantom debt"—debt that is not easily tracked by traditional credit bureaus and can lead individuals into "debt spirals". Public interest in regulation is high, with a significant volume of search queries asking, "Why is BNPL not regulated?" and "Can it impact my credit score?".

Regional Regulatory Shifts (2025-2026)

The narrative pressure regarding "phantom debt" and consumer harm has led to a global wave of regulation.

| Region | Regulatory Status (2025-2026) | Key Requirements for Providers |

| Australia | Effective June 10, 2025 | Hold an Australian Credit License (ACL); join AFCA; follow modified RLOs |

| United Kingdom | Regulation begins July 15, 2026 | Authorization for consumer credit activities; compliance with FCA rules; entry into DPC TPR |

| United States | Increasing scrutiny | Focus on transparency and potential impact on credit reporting |

In Australia, the reforms classify BNPL products as "low-cost credit contracts" (LCCC), mandating that providers verify a customer's financial situation before approval. For purchases under $2,000 AUD, providers can opt into a "scaled-down" responsible lending framework, but they must still perform basic checks. This shift in the regulatory landscape is a direct response to the narrative of "unsustainable spending" that social listening tools identified as a growing consumer concern as early as 2022.

For finance brands, social listening is now a critical risk and compliance capability: it surfaces the narratives that harden into regulatory pressure, enabling teams to detect reputational exposure, consumer harm signals, and policy risk long before they translate into formal oversight.

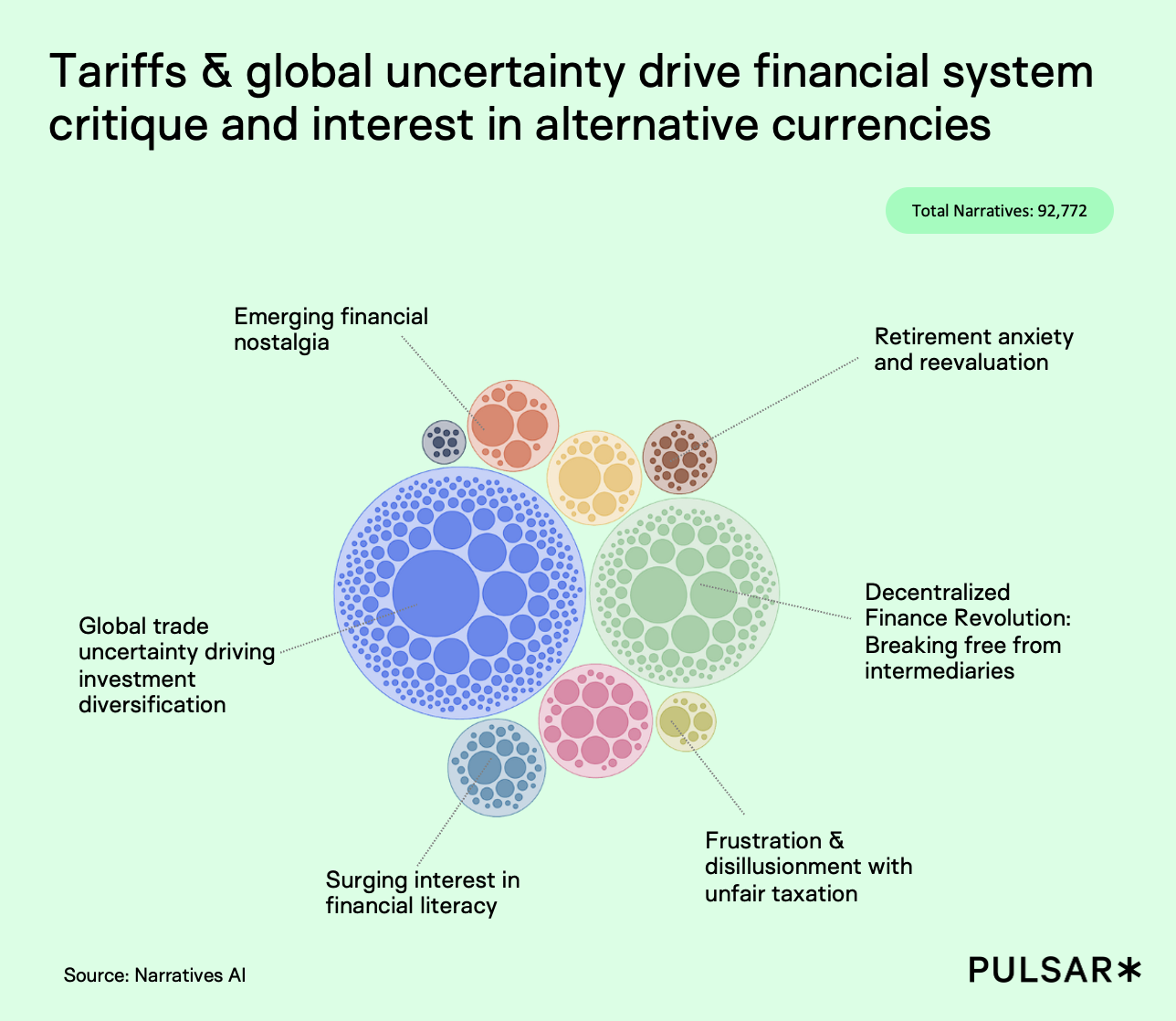

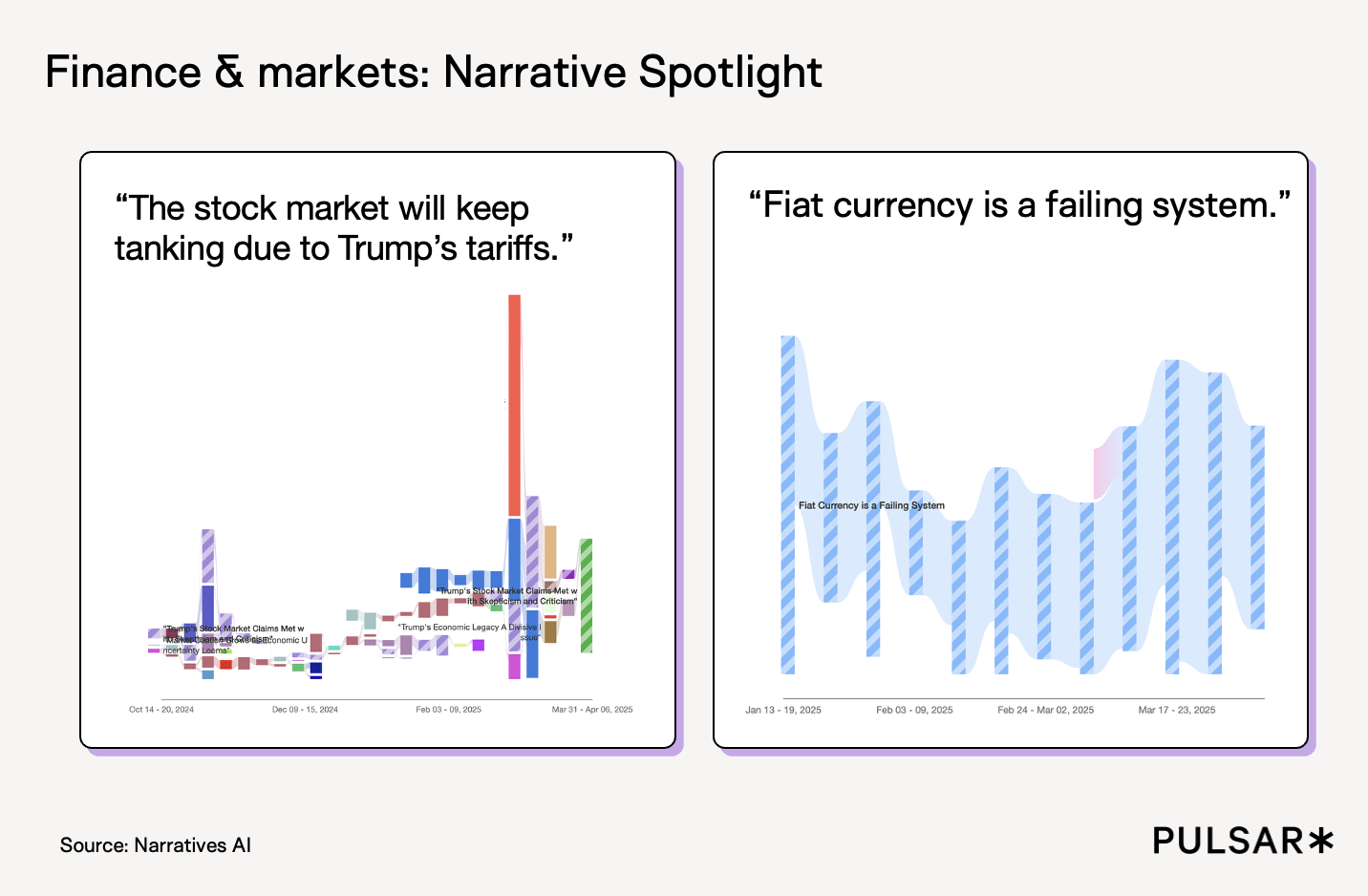

Alternative Currencies and the Distrust of Fiat

Pulsar’s Narrative Report SS25 highlights a fundamental decoupling of the public from traditional monetary systems. Based on an analysis of over 92,000 narratives, the report identifies an intensifying anxiety regarding fiat currency, which is increasingly viewed as a tool for "enriching the elite" rather than a stable store of value.

The DeFi Revolution and the Role of Bitcoin

As trust in central banks remains at a standstill, the "DeFi Revolution" has gained momentum. This movement is driven by a desire to break free from traditional financial intermediaries. Within this narrative, Bitcoin has emerged as a uniquely "trusted" asset because of its fixed supply, which provides a psychological hedge against the perceived "deliberate devaluation" of the U.S. dollar.

While "flashier" assets like memecoins or certain Ethereum-based projects are still discussed, the core narrative for 2025 focuses on "investment diversification" as a means of protection from global trade uncertainty and the impact of tariffs and taxation. This skepticism is fueled by a sense that the "status quo" is no longer serving the public good, especially when basic staples become unaffordable.

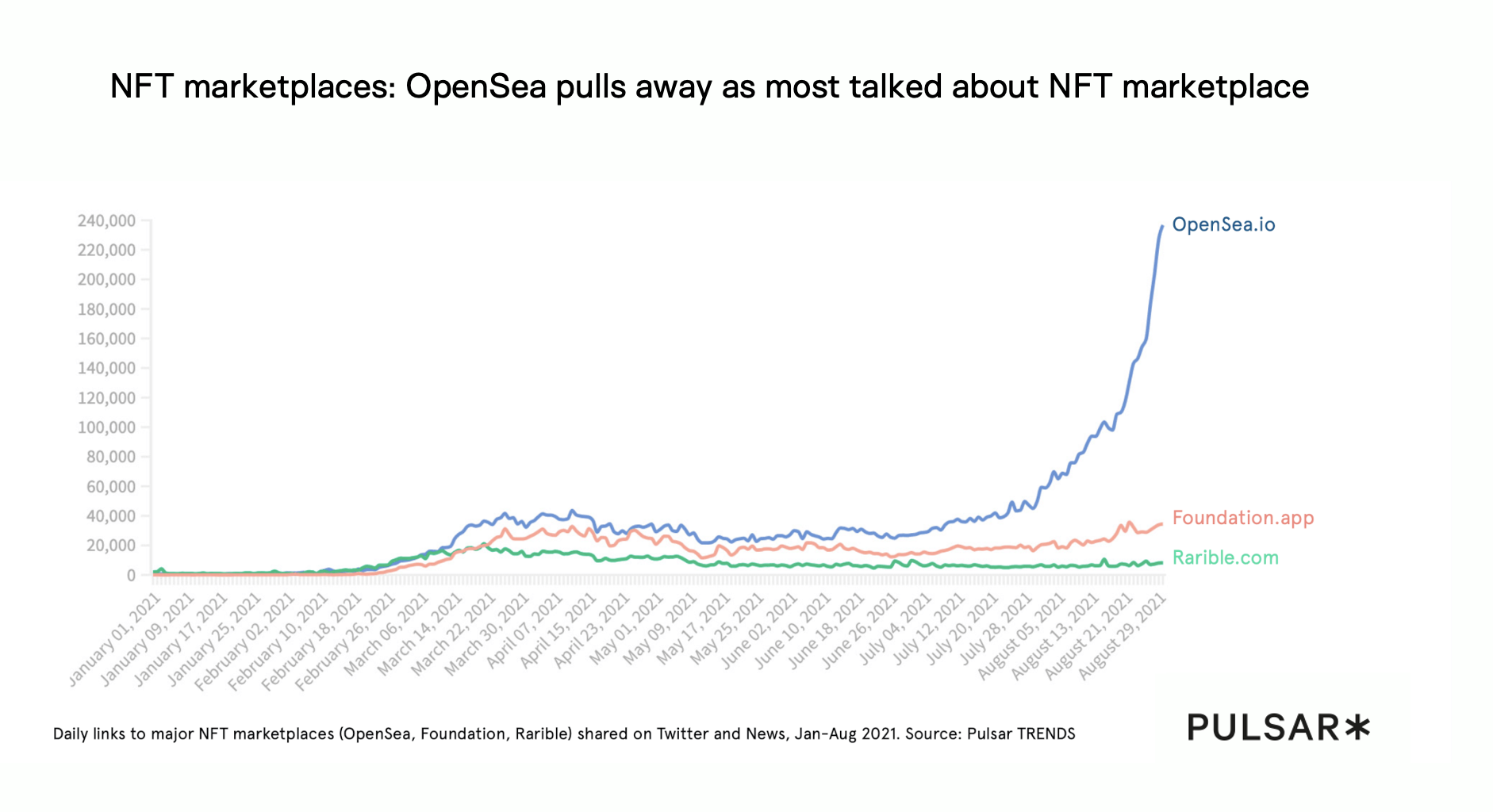

NFTs as a Gateway to Digital Ownership

The entry of NFTs into the mainstream in 2021 was a precursor to this broader shift toward digital autonomy. We researched the online conversation at the explosion of NFTs. By transforming blockchain technology into a medium for collectible "character series" like Bored Ape Yacht Club or CryptoPunks, creators were able to build "active ambassadors" who treated their digital assets with the same reverence as sports trading cards.

Visa's purchase of a CryptoPunk for $150,000 was a watershed moment in this narrative.7 For a legacy financial brand, this was not just an investment but a marketing strategy to earn "cultural respect" from a younger, crypto-native audience. Interestingly, while the move was highly engaged with by the "overall" NFT audience, it did not resonate as strongly with specific sub-communities like Twitch and YouTube streamers, who prioritized celebrity entries (like the YouTuber KSI) over corporate ones. This nuance highlights why high-level audience intelligence is required to measure the true "resonance" of a brand action.

AI and the Future of Financial Experience

Artificial Intelligence is no longer a future trend but a present reality that is reshaping how consumers interact with financial services. According to Deloitte, in 2025, more than 53% of consumers are regularly using or experimenting with Generative AI—a sharp increase from the previous year.

The Mainstreaming of GenAI

Consumers are integrating GenAI into their everyday lives for personal, professional, and educational use, with 42% of regular users reporting a "very positive" effect on their lives. For financial institutions, this represents both an opportunity for "hyper-personalization" and a significant risk regarding trust and data security.

- Shadow AI in the Workplace: Nearly 7 in 10 workers who use GenAI on the job reliance on their own personal tools rather than company-sanctioned versions. This creates a massive compliance gap for financial firms that must manage sensitive data.

- Trust as a Product Feature: Consumers are increasingly wary of how AI is being used ethically. According to Salesforce, trust in businesses using AI correctly fell from 58% in 2023 to 42% in 2025. For tech-driven financial providers, "transparency, explainability, and strong data protection" must be embedded directly into the product experience, not just mentioned in a policy document.

The Framework of Intelligence: Listen, Map, and Activate

To effectively navigate this terrain, financial organizations must adopt a rigorous methodology that transforms raw data into strategic foresight. The Pulsar framework—consisting of the Listen, Map, and Activate stages—provides a comprehensive roadmap for integrating social and narrative intelligence into the core of brand strategy. This model moves beyond the superficial metrics of volume and sentiment, focusing instead on the "why" behind consumer actions and the connections between seemingly disparate conversational data points.

The Listen Phase: Capturing the Unfiltered Voice

The first stage of the process involves establishing a robust infrastructure for data collection that extends far beyond branded mentions and hashtags. In the finance sector, the "Listen" phase requires monitoring a vast array of keywords, including broader industry terms, competitor movements, and cultural conversations that resonate with target segments. High-level intelligence tools now allow for the tracking of nuanced conversations across 195 countries and in all major languages, incorporating data from traditional social platforms like Reddit, Instagram, and X, as well as territory-specific sources like VK, Naver, and Weibo.

A critical component of effective listening is the ability to identify and monitor specific social panels or personas—such as "tech journalists," "millennials," or "basketball fans"—over time to track evolving signals and trends. For financial brands, this might involve creating dedicated panels for "Wannabe VCs," "Young Crypto Enthusiasts," or "First-Time Homebuyers" to understand how these groups perceive market shifts differently. By capturing these unfiltered exchanges, brands can surface truths that surveys often fail to capture, providing a real-time window into cultural shifts.

The Map Phase: Synthesizing Data into Narrative

Once the data is collected, the "Map" phase involves synthesizing these data points into coherent narratives and audience segments based on affinity rather than just demographics. This is where the strategic value of social listening is truly unlocked. Instead of viewing an audience as a monolithic block defined by age or location, narrative intelligence segments users by shared likes, influencers, and behaviors.

This phase employs advanced analytics to connect conversational data points to broader cultural beliefs and trends. For instance, mapping the "emotional and psychological landscape" of an audience allows a brand to understand the root causes of skepticism toward central banks or the sudden surge in interest for "phantom debt" solutions in the Buy Now, Pay Later (BNPL) sector. Tools like Pulsar Narratives enable brands to visualize the relationships between topics, identifying how a political conversation might suddenly spill over into a brand reputation crisis.

The Activate Phase: Translating Insights into Value

The final stage, "Activate," is the process of applying mapped insights to the overall business strategy. This involves moving beyond observation to implementation, where data informs real-time campaign adjustments, long-term product roadmaps, and proactive crisis management. In the context of finance, activation might manifest as the development of an educational content series to address specific "trust barriers" identified in the mapping phase, such as confusion over fee structures or risks associated with new investment products.

Conclusion: Why Social Listening Is Now Essential for Finance Brands

For finance brands, social listening has become a strategic necessity rather than a marketing add-on. Audience and narrative intelligence enable organisations to move beyond campaign-led thinking and instead monitor how trust, risk, and financial behaviour are shaped in real time across digital communities.

By tracking how narratives around performance, governance, consumer harm, and transparency emerge and escalate, finance teams can identify reputational and regulatory pressure before it reaches mainstream media or policymakers. This is particularly critical in lending and BNPL markets, where “phantom debt” and affordability concerns have already translated into formal oversight.

Social listening also provides early insight into longer-term shifts in consumer psychology, including growing interest in alternative finance, decentralisation, and financial autonomy. Understanding these narratives allows brands to respond with credibility rather than speculation.

In an increasingly volatile and regulated financial landscape, social listening underpins the new standard of financial intelligence—connecting audience insight, narrative risk, and strategic decision-making to protect reputation and build durable trust at scale.

To stay up to date with our latest insights and releases, sign up to our newsletter below: