Will Revenge Buying be a Thing Post-Lockdown?

Behavioural science, marketing and consumer psychology are accustomed to terms such as impulse purchasing, conspicuous consumption and, most recently, panic buying. But a new phenomenon seems to have been gaining traction as Covid-19 lockdown begins to ease around the world: revenge spending or revenge buying.

https://twitter.com/_soniashenoy/status/1263327290332717062

This term was initially coined in 2011, describing signs of revenge spending that date back to the 1980s — specifically within China. It relates to how the nation came out of long-term hunger, and into food and restaurant sprees that overwrote the past experience. Today, it is used to describe wealthy or spendthrift consumers' urge to spend money that they couldn't spend on luxury brands when lockdown prevented them from accessing flagship stores, and all the experience that entails. In 2020, we've started to see this pent-up demand in action at the Hermès' Guangzhou store reopening.

For the Global Retail Industry, the question is whether this trend will hold up and become part of our marketing lexicon. In my view, it is doubtful the term will continue for the long-term, given how such behaviour is already understood as impulse purchasing or derivatives. From a behavioural science perspective, revenge buying could be argued to be a negative phrase that, in turn, means consumers are unlikely to adopt and attribute to their behaviour. This ultimately will make it hard to track unless research is done with specific stimulus to probe this behaviour. Still, these issues to one side, the emergence of the trend over COVID-19 is very interesting to both the retail sector and researchers.

What does revenge spending mean to consumers?

Language is important to our understanding of the phenomenon: “revenge” is an action to benefit someone in recompense for something harmful/hurtful done to them. However, when spending money is the action, revenge buying becomes a misnomer — especially when the action of revenge involves a direct "loss", which is money in this case. Currently, the phrase is used in the retail and marketing world as an observation translating to increased sales in China. But considering that consumers are the ones who spend money in “vengeance” within this description, people will be less likely to call their purchases "revenge" buys. Therefore, understanding this phenomenon brings a need for increased sophistication in research design around the topic.

https://www.instagram.com/p/B_AbBoPAaZx/

To date, revenge-buying has been associated with a niche and affluent consumer group that is motivated by status, prestige and self image enhanced with material possessions. This means that when it comes to revenge buying data, not only is the social data volume negligible because of the terminology itself, it’s also limited to retail-publications’ owned conversation on social media. The average consumer population outside wealthy countries like China and the United Arab Emirates (where we see increased volumes of revenge buying buzz) may not practice revenge buying for luxury products after all.

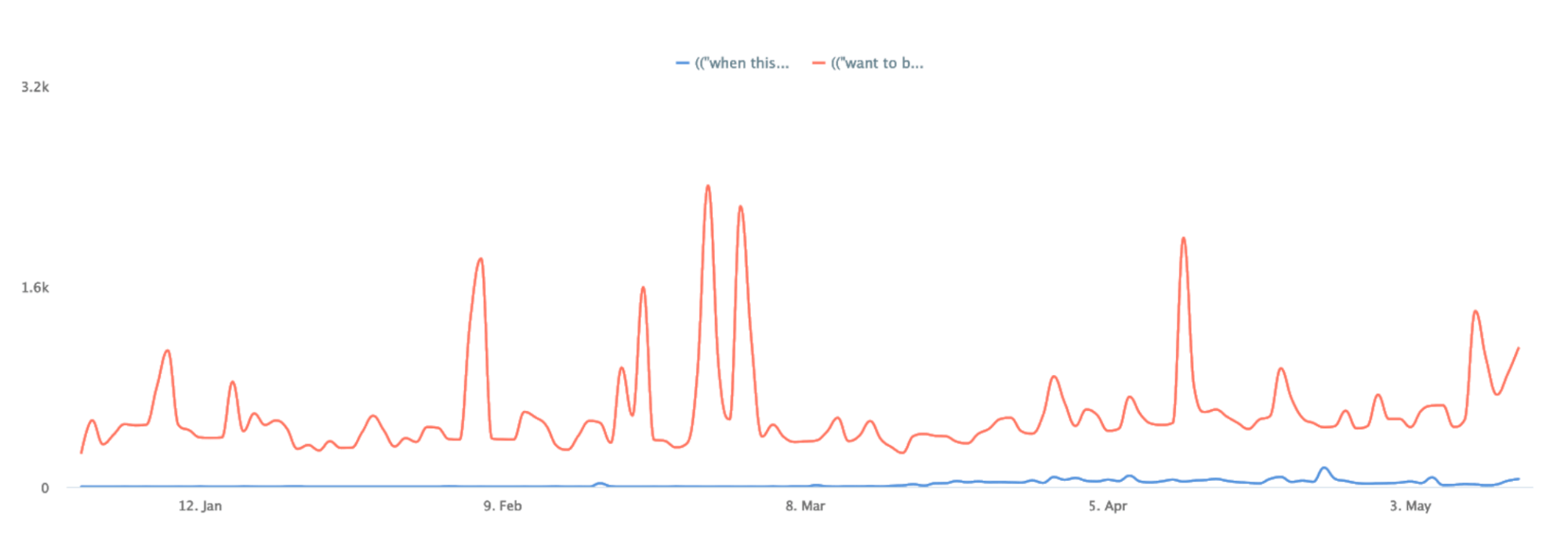

Post-lockdown specific shopping intent vs. generic shopping intent since the beginning of the year - latter shows a consistent presence amongst consumers.

To understand the triggers and urges behind “revenge buying”, it’s important to explore how consumers talk about similar buying behaviour — behaviour that they don’t mind owning and talking about. When we look at global social media conversations for purchase/shopping intent, retail therapy plans, shopping spree urges or anticipation to spend saved money, Pulsar data shows that there is growing buzz coming from the worldwide consumers in general. So what we can monitor is a Covid-19-induced willingness or impulse for more daily/material “gratification”, and desire for the pleasures of shopping, rather than use industry lingo and terminology which may have semantically negative connotations.

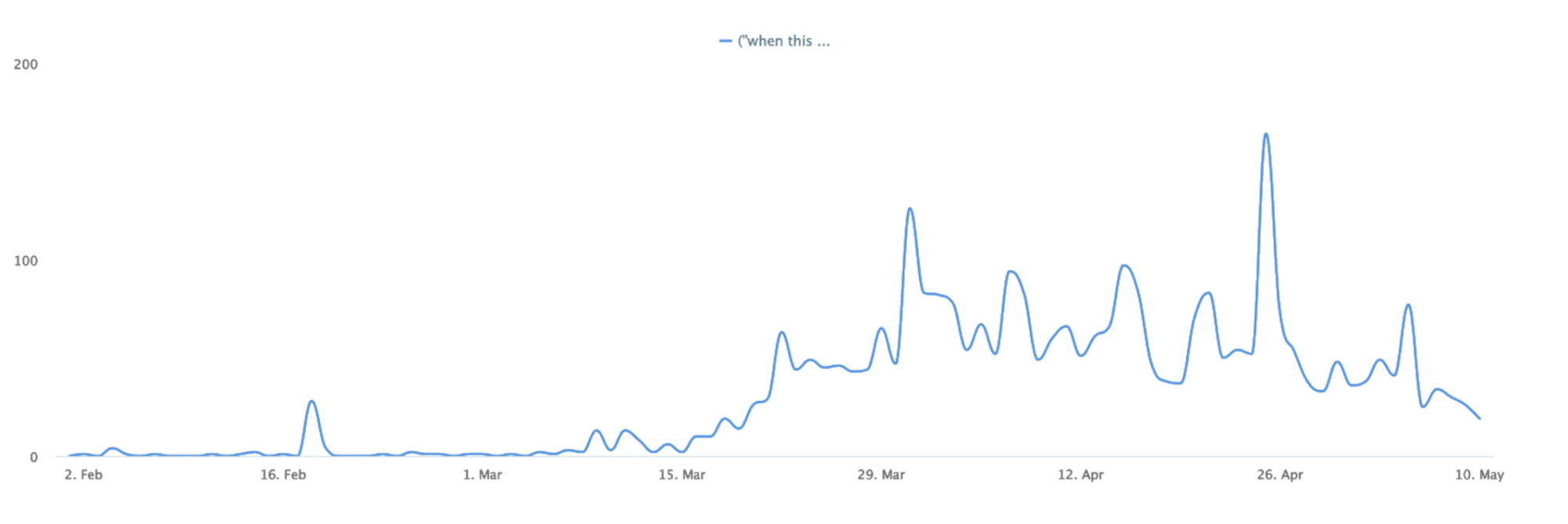

“When this is over…”

As consumers get “itchier” to go back to their normal lives, which our data detects to be increasing especially from mid-March 2020 onwards, more conversations are being shared about what people wish, hope and plan to buy “when the lockdown is over”. This coincides with the time when a number of countries started to share plans to ease or lift lockdown in some areas of society from mid to late March 2020.

https://www.instagram.com/p/CAdU4bngt4f/

Clearly, this has unleashed consumers' plans to go back to normal routines, or get back the shopping pleasures/treats they would normally have. The so-called “lockdown fatigue” is sinking in for a lot of consumers and a new layer of impatience has been added on to their post-lockdown plans, as numerous countries’ lockdown exit plans started to get increased airtime across global media outlets.

“When this is over” themed post-lockdown shopping plans content is low in volume, however vocalisation of plans saw a consistent climb in the last couple of months.

The conversations and engagement around the “when this is/the lockdown is over” and shopping theme saw about 440% increase from 15th March to the highest peak we saw on 25th April — literally from a handful to thousands and counting today. So we can monitor how consumers continue to plan to buy things, but also what they plan to buy or treat themselves with when the lockdown is over. This includes everything from booking luxury holidays to weekend getaways, the latest gaming consoles and wearable fitness tech, all the way to buying new clothes, shoes and accessories — even cars.

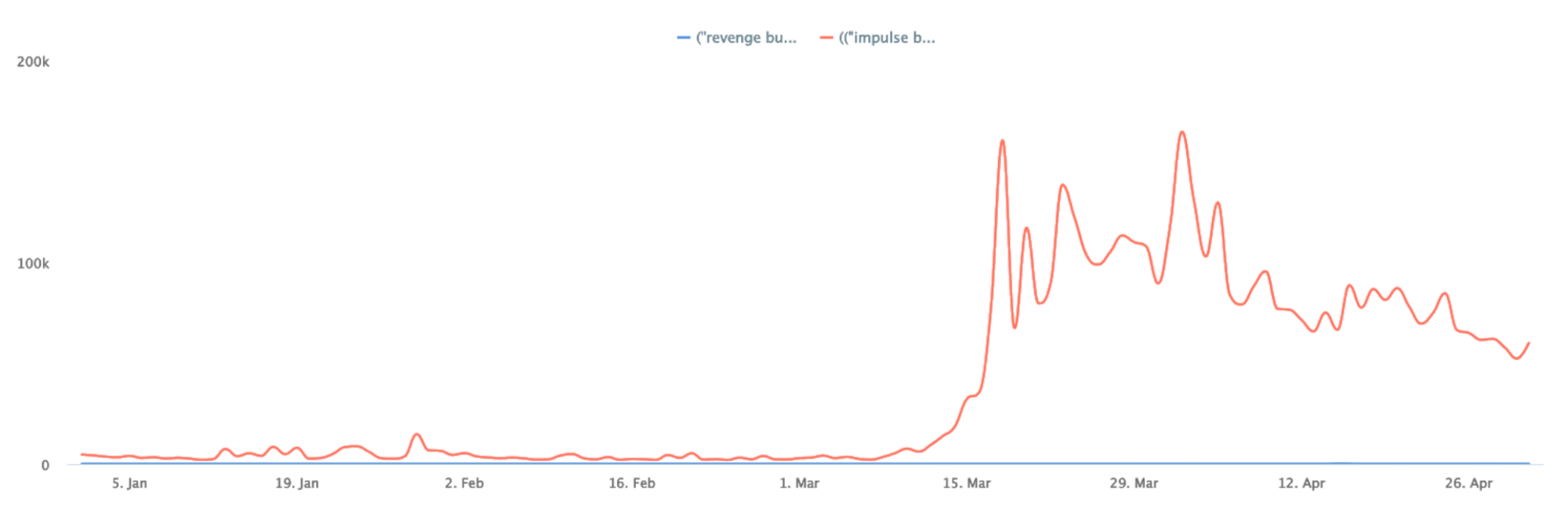

When we investigated “impulse purchasing”, which is a more widespread conversation driver for online purchases according to our data, we saw a consistent and similar trend line amongst consumers. Similar to the “when this is over” conversations, mid-March onwards is when we see consumers owning the impulse purchase conversations and sharing what they bought in lockdown/look to buy in the future. The need for consumers to feel good in a low-stimulus lockdown environment meant that they aren’t just planning for post-lockdown shopping out of boredom and fatigue, they are also likely to have more savings than usual because they spend less during lockdown.

Revenge buying related conversations are almost non-existent, while impulse buying/purchasing related content proves to be a better signal for consumer usage and engagement, showing over 350% increase in volume on and after March 15.

Revenge buying vs treating oneself vs impulse purchases

Thinking about the niche affluent consumers who are observed to be revenge buying, it’s likely that a) they will not talk about it as much as the average consumer would on social media given they are used to luxury, and b) once the lockdown has passed, they will just go back to their regular luxury-led frequent shopping behaviour. This means that this surge seen in China is likely to just blend into general affluent consumer behaviour elsewhere in the world and not remain “a thing”. On the other hand, general behavioural signals around impulse purchases or “treating oneself” — especially when freedom of shopping is restricted — will remain a part of our day-to-day because both of these phenomena can result from various restrictions or changes in consumers’ individual lives anyway.

Our analysis shows how important it is that researchers and retailers alike put themselves in the shoes of their customer and start with behavioural signals and their derivatives when analysing data. “Treating oneself” in times of deprivation of any kind (lockdown meant inability to meet friends and family, closure of shops etc.) is a phenomenon that will remain as long as Covid-19 continues to spread. As a result, we can say that online retail could continue to see increased demand not just for essentials but for things that make consumers feel good about themselves, their immediate surroundings and the rest of the world.

https://twitter.com/benoobrown/status/1263154459804385282

When the lockdown is indeed over, it's likely that we will see many of consumers' shopping plans turn to reality — so we will see increased footfall and spend offline too. Of course, it's highly possible that this will be a brief phase before consumers revert to being very careful with money. Nonetheless, these trends present the retail sector with positive opportunities to re-engage consumers and tap into latent shopping motivations.